Blank Seller Utah Form

Blank Seller Utah Form

The Seller Financing Addendum to the Real Estate Purchase Contract (REPC) is a crucial document for buyers and sellers engaging in a real estate transaction in Utah. This addendum outlines the specific terms under which the seller agrees to provide financing to the buyer, thereby facilitating a smoother transaction process. Key components of the form include the identification of credit documents, which may consist of a note and deed of trust or an all-inclusive deed of trust. It details the credit terms, such as the principal amount, interest rate, payment schedule, and any balloon payments that may be required. Additionally, the addendum stipulates the responsibilities of the buyer concerning property taxes, homeowners association dues, and insurance premiums, ensuring that all financial obligations are clearly understood. The payment section specifies where and how payments will be made, while provisions regarding late payments and prepayments are also included to protect both parties. Importantly, the addendum includes a due-on-sale clause, which can impact the buyer's obligations should the underlying mortgage be called due. The seller's approval process is clearly outlined, requiring the buyer to provide financial disclosures and a credit report. Finally, the document emphasizes the importance of transparency by mandating the exchange of tax identification numbers. By addressing these essential aspects, the Seller Financing Addendum serves to protect the interests of both buyers and sellers while promoting a clear understanding of their respective rights and responsibilities.

Medical Power of Attorney Utah - This directive serves as a vital part of advance care planning in Utah.

A Missouri Non-disclosure Agreement (NDA) is a legal document designed to protect confidential information shared between parties. By outlining the terms of confidentiality, this form helps prevent unauthorized disclosure of sensitive data. To ensure your information remains secure, consider filling out the NDA form by clicking the button below or by accessing Missouri PDF Forms for more resources.

Advance Directive Utah - Your choices in this form reflect your personal values and desires concerning health care decisions.

Dws-esd 631 - It is designed for employers to file quarterly wage information.

| Fact Name | Details |

|---|---|

| Form Purpose | This form serves as a Seller Financing Addendum to a Real Estate Purchase Contract in Utah. |

| Governing Law | The form is governed by the laws of the State of Utah, specifically the regulations set forth by the Utah Real Estate Commission. |

| Credit Documentation | Seller financing is evidenced through various credit documents, including a Note and Deed of Trust or an All-Inclusive Deed of Trust. |

| Tax Responsibilities | Buyers are responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums. |

| Late Payment Terms | Payments made after the due date may incur a late charge, and the principal may be paid early without penalty. |

| Disclosure Requirements | Both Buyer and Seller must disclose their Social Security Numbers or tax identification numbers by Settlement for compliance with federal laws. |

In real estate transactions, various forms and documents accompany the Seller Utah form to ensure that all parties understand their rights and obligations. Each of these documents plays a critical role in facilitating the sale and financing of property. Below is a list of commonly used forms that often accompany the Seller Utah form, along with a brief description of each.

These documents work together to create a comprehensive framework for the real estate transaction. They help protect the interests of both buyers and sellers while facilitating a smooth transfer of property ownership. Understanding each of these forms is essential for anyone involved in a real estate transaction in Utah.

Filling out the Seller Financing Addendum to the Real Estate Purchase Contract in Utah can be a daunting task. Many individuals make common mistakes that can lead to confusion or even legal complications. Here are ten frequent errors to avoid when completing this important document.

One significant mistake is failing to accurately fill in the Offer Reference Date. This date is crucial as it establishes the timeline for the agreement. If left blank or incorrectly filled, it can create uncertainty about when the contract takes effect.

Another common error is neglecting to specify the principal amount of the note in Section 2. This figure should be clear and precise. Omitting this information can lead to disputes over the amount owed, complicating the transaction.

Many sellers also forget to include the interest rate in the credit terms. This omission can have serious financial implications. Buyers need to understand how much interest they will be paying over time to make informed decisions.

In Section 3, some individuals fail to indicate how property taxes and assessments will be paid. It's essential to clarify whether these will be paid directly to the seller, an escrow agent, or another entity. This detail helps avoid misunderstandings about financial responsibilities.

Another frequent mistake involves the payment recipient in Section 4. Sellers should clearly indicate whether payments will go to them directly or to an escrow agent. Confusion in this area can lead to missed payments and strained relationships.

When it comes to late payments, sellers often neglect to specify the grace period before late fees apply. It's important to define this time frame to avoid disputes later on. Buyers should know exactly how many days they have before incurring additional charges.

In Section 6, some sellers overlook the requirement to provide the underlying mortgage documents to the buyer. This step is essential for transparency and helps buyers understand any existing obligations tied to the property.

Buyers sometimes fail to submit the Buyer Financial Information Sheet as required in Section 7. This document is critical for the seller to assess the buyer's financial capability. Not providing it can delay the process or even jeopardize the sale.

Another common mistake occurs in Section 9, where buyers may forget to indicate whether they will provide a lender's policy of title insurance. This policy protects both parties, and its absence can create complications during the settlement process.

Lastly, many sellers and buyers neglect to disclose their Social Security Numbers or tax identification numbers as required in Section 10. This information is necessary for compliance with federal reporting laws. Failing to provide it can lead to legal issues down the line.

By being aware of these common mistakes, individuals can approach the Seller Financing Addendum with greater confidence and clarity. Attention to detail can make a significant difference in ensuring a smooth transaction.

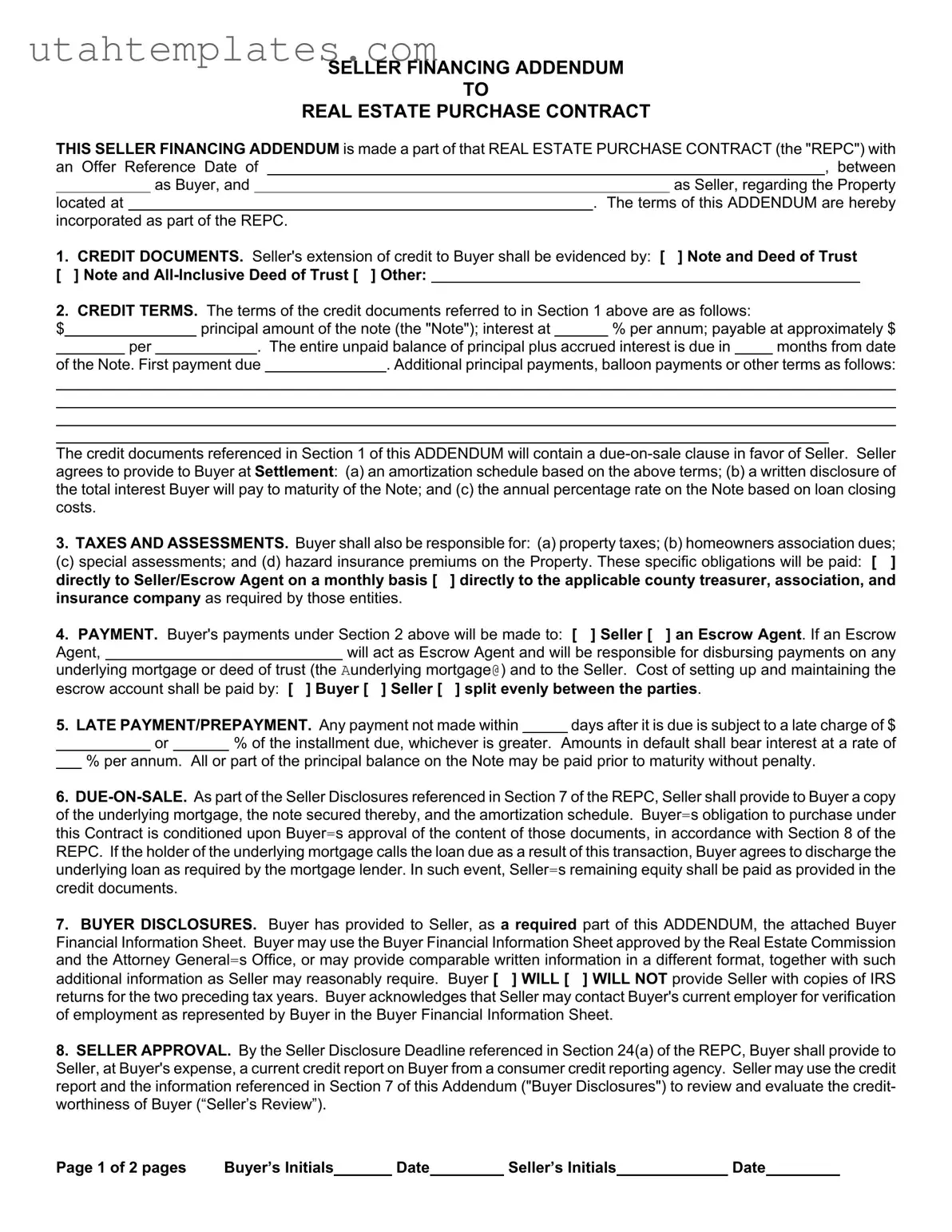

SELLER FINANCING ADDENDUM

TO

REAL ESTATE PURCHASE CONTRACT

THIS SELLER FINANCING ADDENDUM is made a part of that REAL ESTATE PURCHASE CONTRACT (the "REPC") with

an Offer Reference Date of |

|

|

|

, between |

|||

|

|

as Buyer, and |

|

|

as Seller, regarding the Property |

||

located at |

|

. The terms of this ADDENDUM are hereby |

|||||

incorporated as part of the REPC. |

|

|

|

||||

1. CREDIT DOCUMENTS. Seller's extension of credit to Buyer shall be evidenced by: [ ] Note and Deed of Trust [ ] Note and

2.CREDIT TERMS. The terms of the credit documents referred to in Section 1 above are as follows:

$ |

|

|

principal amount of the note (the "Note"); interest at |

|

% per annum; payable at approximately $ |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

per |

|

|

. The entire unpaid balance of principal plus accrued interest is due in |

|

months from date |

|||||

of the Note. First payment due |

|

. Additional principal payments, balloon payments or other terms as follows: |

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

The credit documents referenced in Section 1 of this ADDENDUM will contain a

3.TAXES AND ASSESSMENTS. Buyer shall also be responsible for: (a) property taxes; (b) homeowners association dues;

(c) special assessments; and (d) hazard insurance premiums on the Property. These specific obligations will be paid: [ ] directly to Seller/Escrow Agent on a monthly basis [ ] directly to the applicable county treasurer, association, and insurance company as required by those entities.

4. PAYMENT. Buyer's payments under Section 2 above will be made to: [ ] Seller [ ] an Escrow Agent. If an Escrow

Agent,will act as Escrow Agent and will be responsible for disbursing payments on any

underlying mortgage or deed of trust (the Aunderlying mortgage@) and to the Seller. Cost of setting up and maintaining the escrow account shall be paid by: [ ] Buyer [ ] Seller [ ] split evenly between the parties.

5. LATE PAYMENT/PREPAYMENT. Any payment not made within |

|

|

days after it is due is subject to a late charge of $ |

|||

|

or |

|

% of the installment due, whichever is greater. |

Amounts in default shall bear interest at a rate of |

||

%per annum. All or part of the principal balance on the Note may be paid prior to maturity without penalty.

6.

7.BUYER DISCLOSURES. Buyer has provided to Seller, as a required part of this ADDENDUM, the attached Buyer Financial Information Sheet. Buyer may use the Buyer Financial Information Sheet approved by the Real Estate Commission and the Attorney General=s Office, or may provide comparable written information in a different format, together with such

additional information as Seller may reasonably require. Buyer [ ] WILL [ ] WILL NOT provide Seller with copies of IRS returns for the two preceding tax years. Buyer acknowledges that Seller may contact Buyer's current employer for verification of employment as represented by Buyer in the Buyer Financial Information Sheet.

8.SELLER APPROVAL. By the Seller Disclosure Deadline referenced in Section 24(a) of the REPC, Buyer shall provide to Seller, at Buyer's expense, a current credit report on Buyer from a consumer credit reporting agency. Seller may use the credit report and the information referenced in Section 7 of this Addendum ("Buyer Disclosures") to review and evaluate the credit- worthiness of Buyer (“Seller’s Review”).

Page 1 of 2 pages |

Buyer’s Initials |

|

Date |

Seller’s Initials |

Date |

|||

|

|

|

|

|

|

|

|

|

8.1Seller Review. If Seller determines, in Seller’s sole discretion, that the results of the Seller’s Review are unacceptable, Seller may either: (a) no later than the Due Diligence Deadline referenced in Section 24(b) of the REPC, cancel the REPC by providing written notice to Buyer, whereupon the Earnest Money Deposit shall be released to Buyer without the requirement of further written authorization from Seller; or (b) no later than the Due Diligence Deadline referenced in Section 24(b), resolve in writing with Buyer any objections Seller has arising from Seller’s Review.

8.2Failure to Cancel or Resolve Objections. If Seller fails to cancel the REPC or resolve in writing any objections Seller has arising from Seller’s Review, as provided in Section 8.1 of this ADDENDUM, Seller shall be deemed to have waived the Seller=s Review.

9.TITLE INSURANCE. Buyer [ ] SHALL [ ] SHALL NOT provide to Seller a lender=s policy of title insurance in the amount of the indebtedness to the Seller, and shall pay for such policy at Settlement.

10.DISCLOSURE OF TAX IDENTIFICATION NUMBERS. By no later than Settlement, Buyer and Seller shall disclose to each other their respective Social Security Numbers or other applicable tax identification numbers so that they may comply with federal laws on reporting mortgage interest in filings with the Internal Revenue Service.

To the extent the terms of this ADDENDUM modify or conflict with any provisions of the REPC, including all prior addenda and counteroffers, these terms shall control. All other terms of the REPC, including all prior addenda and counteroffers, not

modified by this ADDENDUM shall remain the same. [ ] Seller [ ] Buyer shall have until |

|

[ ] AM [ ] PM |

||

Mountain Time on |

|

(Date), to accept the terms of this SELLER FINANCING ADDENDUM in |

||

accordance with Section 23 of the REPC. Unless so accepted, the offer as set forth in this SELLER FINANCING ADDENDUM shall lapse.

_________________________________________________________________________________________________

[ ] Buyer [ ] Seller Signature(Date) (Time)Social Security Number

_________________________________________________________________________________________________

[ ] Buyer [ ] Seller Signature |

(Date) (Time) |

Social Security Number |

ACCEPTANCE/COUNTEROFFER/REJECTION

CHECK ONE:

[ ]ACCEPTANCE: [ ] Seller [ ] Buyer hereby accepts these terms.

[]COUNTEROFFER: [ ] Seller [ ] Buyer presents as a counteroffer the terms set forth on the attached ADDENDUM NO.

______.

[]REJECTION: [ ] Seller [ ] Buyer rejects the foregoing SELLER FINANCING ADDENDUM.

(Signature) |

(Date) |

(Time) |

(Signature) |

(Date) |

(Time) |

|

|

|

|

|

|

(Signature) |

(Date) |

(Time) |

(Signature) |

(Date) |

(Time) |

THIS FORM APPROVED BY THE UTAH REAL ESTATE COMMISSION AND THE OFFICE OF THE UTAH ATTORNEY GENERAL,

EFFECTIVE AUGUST 27, 2008. AS OF JANUARY 1, 2009, IT WILL REPLACE AND SUPERSEDE THE PREVIOUSLY APPROVED VERSION OF THIS FORM.

Page 2 of 2 pages |

Buyer’s Initials |

|

Date |

Seller’s Initials |

Date |

|||

|

|

|

|

|

|

|

|

|

Understanding the Seller Financing Addendum in Utah is crucial for both buyers and sellers involved in real estate transactions. Here are some key takeaways to keep in mind:

By keeping these points in mind, both buyers and sellers can navigate the Seller Financing Addendum more effectively, ensuring a smoother transaction process.