Blank Utah Seller Financing Addendum Form

Blank Utah Seller Financing Addendum Form

The Utah Seller Financing Addendum is an essential document that supplements a Real Estate Purchase Contract (REPC) when the seller agrees to finance the buyer's purchase of a property. This addendum outlines critical details such as the credit documents involved, which may include a note and deed of trust or an all-inclusive deed of trust. It specifies the credit terms, including the principal amount, interest rate, payment schedule, and any balloon payments. Responsibilities for property taxes, homeowners association dues, and hazard insurance premiums are clearly defined, ensuring both parties understand their obligations. Payment methods are also addressed, allowing for direct payments to the seller or through an escrow agent. The addendum includes provisions for late payments and prepayments, as well as a due-on-sale clause that protects the seller's interests. Additionally, it requires the buyer to provide financial disclosures and a credit report for the seller's review, ensuring transparency in the financing process. This document serves as a comprehensive guide for both buyers and sellers, clarifying their rights and responsibilities in the seller financing arrangement.

Utah Cpe - Participating as an instructor or author also counts toward your total CPE hours.

Car Gift - The form contains terms that require responsible record maintenance.

Filing the Indiana Homeschool Letter of Intent is essential for parents who wish to legally homeschool their children, providing a formal notification to the state. To aid in this process, families can refer to resources that offer guidance on completing this form effectively, such as the information available at https://homeschoolintent.com/editable-indiana-homeschool-letter-of-intent, which can simplify the transition into homeschooling.

Utah Dws Sds 305 - Auxiliary aids for individuals with disabilities are mentioned for accommodations.

| Fact Name | Fact Detail |

|---|---|

| Purpose | The Seller Financing Addendum is used to outline the terms of financing provided by the seller to the buyer in a real estate transaction. |

| Incorporation | This addendum becomes part of the Real Estate Purchase Contract (REPC) once agreed upon by both parties. |

| Credit Documents | The seller's credit extension is documented through a Note and Deed of Trust or an All-Inclusive Deed of Trust. |

| Tax Responsibilities | The buyer is responsible for property taxes, homeowners association dues, special assessments, and hazard insurance premiums. |

| Payment Structure | Payments can be made directly to the seller or an escrow agent, as agreed upon in the addendum. |

| Late Payment Terms | Payments made late may incur a charge, either a fixed amount or a percentage of the installment due. |

| Due-On-Sale Clause | This addendum includes a due-on-sale clause, allowing the seller to call the loan due if the property is sold. |

| Buyer Disclosures | The buyer must provide financial information and may need to share IRS returns for verification. |

| Governing Laws | This addendum is governed by Utah law, specifically the regulations set forth by the Utah Real Estate Commission. |

The Utah Seller Financing Addendum is an important document that outlines the terms of seller financing in a real estate transaction. In addition to this addendum, there are several other forms and documents that are commonly used to facilitate the sale and ensure that all parties are informed and protected. Below is a list of these documents, along with brief descriptions of each.

These forms and documents work together to create a comprehensive framework for real estate transactions involving seller financing. Each document plays a specific role in ensuring that both the buyer and seller are informed and protected throughout the process.

Filling out the Utah Seller Financing Addendum form requires attention to detail. One common mistake is failing to accurately complete the credit terms. Buyers often overlook specifying the principal amount, interest rate, and payment schedule. These details are crucial as they determine the financial obligations of the buyer. Incomplete or incorrect entries can lead to confusion and disputes later.

Another frequent error involves the selection of payment recipients. Buyers may neglect to indicate whether payments will be made to the Seller or an Escrow Agent. This choice impacts how funds are managed and distributed. If this section is left blank or filled out incorrectly, it could complicate the payment process.

Additionally, individuals often misinterpret the late payment and prepayment terms. Buyers might not specify the late charge amount or the interest rate for defaulted payments. Such omissions can lead to misunderstandings about penalties and the consequences of missed payments, potentially resulting in financial strain.

Another common mistake is in the due-on-sale clause. Buyers sometimes fail to acknowledge this clause's implications, which can lead to unexpected responsibilities. Understanding that the underlying mortgage may become due if the property is sold is essential for both parties involved.

Buyers may also forget to provide the necessary financial disclosures. The addendum requires a Buyer Financial Information Sheet, and neglecting to include this can delay the process. This information is vital for the seller to assess the buyer's creditworthiness and financial stability.

Moreover, inaccuracies in the title insurance section are common. Buyers might either fail to check the appropriate box regarding the provision of a lender's policy or misunderstand who is responsible for paying for it. This oversight can create complications during the settlement process.

Finally, a significant mistake is not adhering to the acceptance deadline. Buyers or sellers may forget to specify or miss the time and date by which the addendum must be accepted. If this deadline is not met, the offer may lapse, leading to potential loss of the transaction.

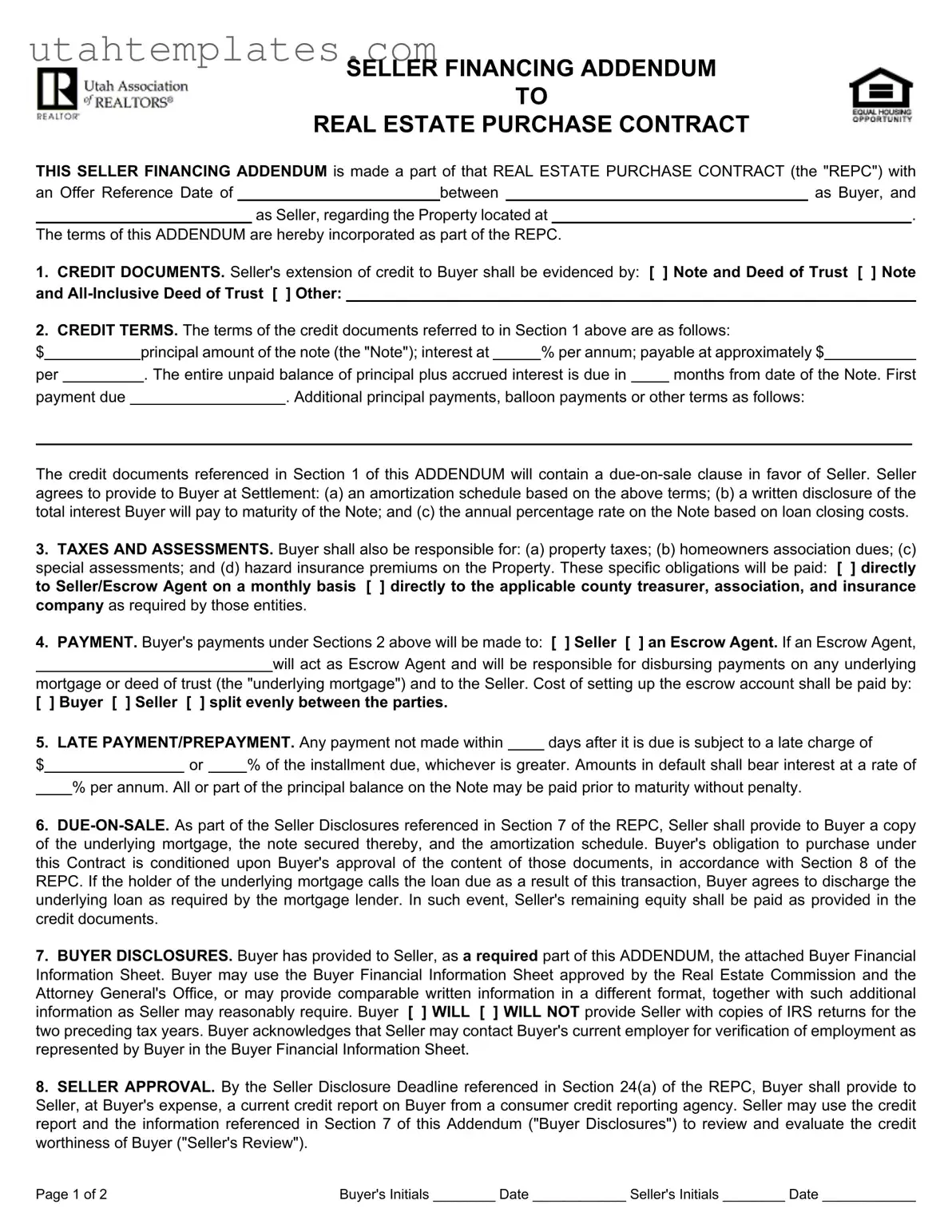

SELLER FINANCING ADDENDUM

TO

REAL ESTATE PURCHASE CONTRACT

THIS SELLER FINANCING ADDENDUM is made a part of that REAL ESTATE PURCHASE CONTRACT (the "REPC") with

an Offer Reference Date of |

|

|

between |

|

as Buyer, and |

||

|

|

as Seller, regarding the Property located at |

|

. |

|||

|

|

|

|

|

|||

The terms of this ADDENDUM are hereby incorporated as part of the REPC. |

|

|

|||||

1.CREDIT DOCUMENTS. Seller's extension of credit to Buyer shall be evidenced by: [ ] Note and Deed of Trust [ ] Note and

2.CREDIT TERMS. The terms of the credit documents referred to in Section 1 above are as follows:

$ |

|

|

principal amount of the note (the "Note"); interest at |

|

% per annum; payable at approximately $ |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

per |

|

|

|

. The entire unpaid balance of principal plus accrued interest is due in |

|

months from date of the Note. First |

|||||

payment due |

|

|

|

. Additional principal payments, balloon payments or other terms as follows: |

|||||||

The credit documents referenced in Section 1 of this ADDENDUM will contain a

3.TAXES AND ASSESSMENTS. Buyer shall also be responsible for: (a) property taxes; (b) homeowners association dues; (c) special assessments; and (d) hazard insurance premiums on the Property. These specific obligations will be paid: [ ] directly to Seller/Escrow Agent on a monthly basis [ ] directly to the applicable county treasurer, association, and insurance company as required by those entities.

4.PAYMENT. Buyer's payments under Sections 2 above will be made to: [ ] Seller [ ] an Escrow Agent. If an Escrow Agent,

will act as Escrow Agent and will be responsible for disbursing payments on any underlying mortgage or deed of trust (the "underlying mortgage") and to the Seller. Cost of setting up the escrow account shall be paid by:

[ ] Buyer [ ] Seller [ ] split evenly between the parties.

5. LATE PAYMENT/PREPAYMENT. Any payment not made within |

|

days after it is due is subject to a late charge of |

||||

$ |

|

or |

|

% of the installment due, whichever is greater. Amounts in default shall bear interest at a rate of |

||

%per annum. All or part of the principal balance on the Note may be paid prior to maturity without penalty.

6.

7.BUYER DISCLOSURES. Buyer has provided to Seller, as a required part of this ADDENDUM, the attached Buyer Financial Information Sheet. Buyer may use the Buyer Financial Information Sheet approved by the Real Estate Commission and the Attorney General's Office, or may provide comparable written information in a different format, together with such additional information as Seller may reasonably require. Buyer [ ] WILL [ ] WILL NOT provide Seller with copies of IRS returns for the two preceding tax years. Buyer acknowledges that Seller may contact Buyer's current employer for verification of employment as represented by Buyer in the Buyer Financial Information Sheet.

8.SELLER APPROVAL. By the Seller Disclosure Deadline referenced in Section 24(a) of the REPC, Buyer shall provide to Seller, at Buyer's expense, a current credit report on Buyer from a consumer credit reporting agency. Seller may use the credit report and the information referenced in Section 7 of this Addendum ("Buyer Disclosures") to review and evaluate the credit worthiness of Buyer ("Seller's Review").

Page 1 of 2 |

Buyer's Initials ________ Date ____________ Seller's Initials ________ Date ____________ |

8.1Seller Review. If Seller determines, in Seller's sole discretion, that the results of the Seller's Review are unacceptable, Seller may either: (a) no later than the Due Diligence Deadline referenced in Section 24(b) of the REPC, cancel the REPC by providing written notice to Buyer, whereupon the Earnest Money Deposit shall be released to Buyer without the requirement of further written authorization from Seller; or (b) no later than the Due Diligence Deadline referenced in Section 24(b), resolve in writing with Buyer any objections Seller has arising from Seller's Review.

8.2Failure to Cancel or Resolve Objections. If Seller fails to cancel the REPC or resolve in writing any objections Seller has arising from Seller's Review, as provided in Section 8.1 of this ADDENDUM, Seller shall be deemed to have waived the Seller's Review.

9.TITLE INSURANCE. Buyer [ ] SHALL [ ] SHALL NOT provide to Seller a lender's policy of title insurance in the amount of the indebtedness to the Seller, and shall pay for such policy at Settlement.

10.DISCLOSURE OF TAX IDENTIFICATION NUMBERS. By no later than Settlement, Buyer and Seller shall disclose to each other their respective Social Security Numbers or other applicable tax identification numbers so that they may comply with federal laws on reporting mortgage interest in filings with the Internal Revenue Service.

To the extent the terms of this ADDENDUM modify or conflict with any provisions of the REPC, including all prior addenda and counteroffers, these terms shall control. All other terms of the REPC, including all prior addenda and counteroffers, not modified

by this ADDENDUM shall remain the same. [ |

] Seller |

[ ] Buyer shall have until |

|

: |

|

[ ] AM [ ] PM Mountain Time |

|||

on |

|

|

(Date), to accept the terms of this SELLER FINANCING ADDENDUM in accordance with Section 23 of |

||||||

the REPC. Unless so accepted, the offer as set forth in this SELLER FINANCING ADDENDUM shall lapse. |

|||||||||

|

|

|

|

|

|

|

|

|

|

[ ] Buyer [ |

] Seller Signature |

(Date) |

(Time) |

|

|

|

Social Security Number |

||

[ ] Buyer [ ] Seller Signature |

(Date) |

(Time) |

Social Security Number |

ACCEPTANCE/COUNTEROFFER/REJECTION

CHECK ONE:

[ ] ACCEPTANCE: [ ] Seller [ ] Buyer hereby accepts the these terms.

[] COUNTEROFFER: [ ] Seller [ ] Buyer presents as a counteroffer the terms set forth on the attached ADDENDUM NO.

[] REJECTION: [ ] Seller [ ] Buyer rejects the foregoing SELLER FINANCING ADDENDUM.

(Signature) |

(Date) |

(Time) (Signature) |

(Date) |

(Time) |

THIS FORM APPROVED BY THE UTAH REAL ESTATE COMMISSION AND THE OFFICE OF THE UTAH ATTORNEY GENERAL, EFFECTIVE AUGUST 27, 2008. AS OF

JANUARY 1, 2009, IT WILL REPLACE AND SUPERCEDE THE PREVIOUSLY APPROVED VERSION OF THIS FORM.

Page 2 of 2 |

Buyer's Initials ________ Date ____________ Seller's Initials ________ Date ____________ |

The Utah Seller Financing Addendum form shares similarities with several other documents commonly used in real estate transactions. Each document serves a specific purpose in facilitating the sale and financing of property. Below are four documents that are similar to the Seller Financing Addendum:

Understanding the Utah Seller Financing Addendum is essential for both buyers and sellers involved in real estate transactions. Here are some key takeaways to keep in mind: