Blank Utah Tc 20 Form

Blank Utah Tc 20 Form

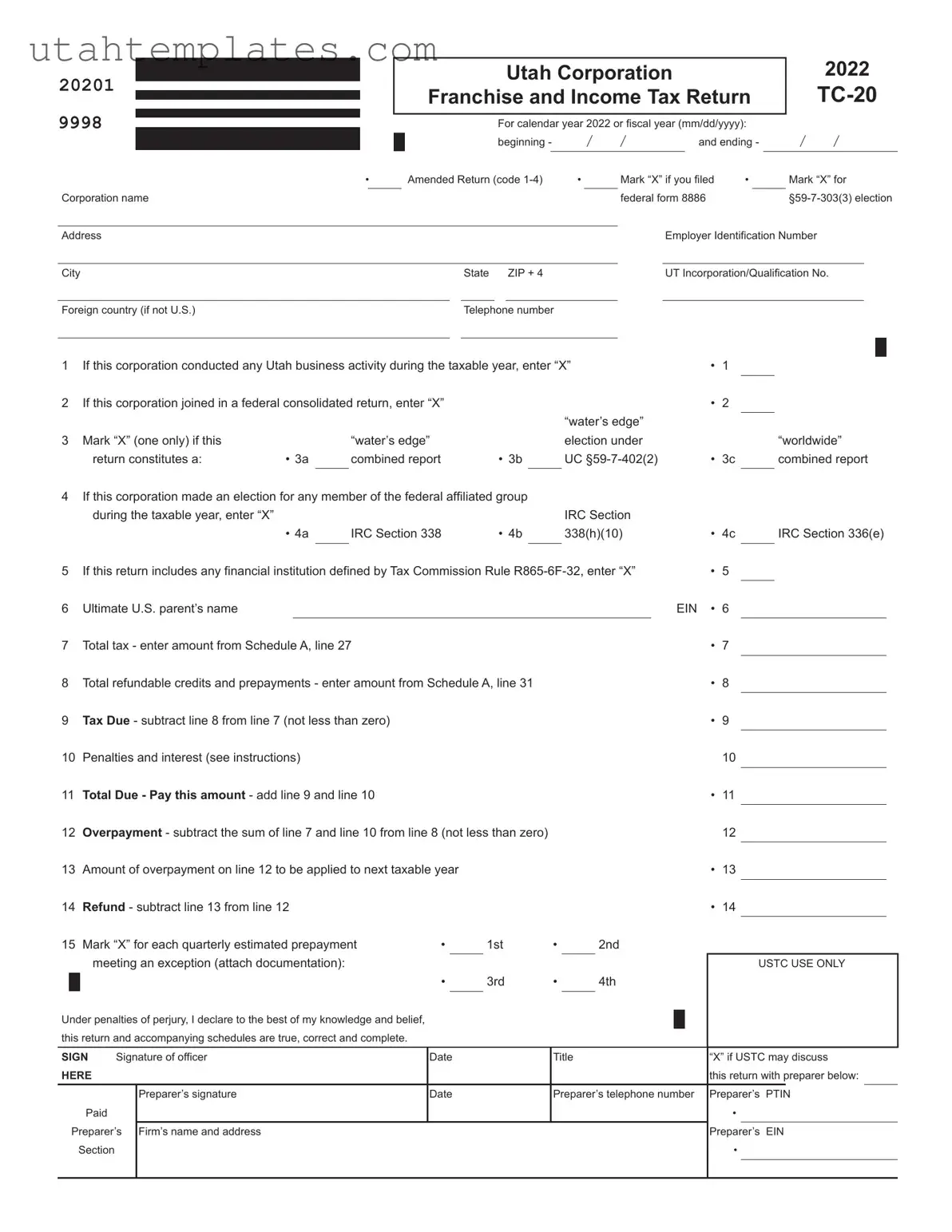

The Utah TC-20 form is a crucial document for corporations operating in Utah, as it serves as the Franchise and Income Tax Return for the year 2020. This form is designed to capture essential information about the corporation's financial activities within the state. It requires the corporation to provide its name, address, Employer Identification Number, and details regarding its business activities in Utah. Corporations must indicate whether they are filing an amended return or if they have joined in a federal consolidated return. Additionally, the form includes sections for tax calculations, reporting of refundable credits, and any penalties or interest that may apply. Notably, the TC-20 form also asks for information about ownership structures, changes in control, and the location of corporate records. Each section is carefully structured to ensure that all relevant financial data is accurately reported, facilitating the state's ability to assess tax obligations effectively. Understanding how to complete the TC-20 form is vital for compliance and can significantly impact a corporation's financial standing.

Utah State Withholding - The form serves as a reconciliation tool for employers with discrepancies in their tax reporting.

In addition to completing the essential Indiana Homeschool Letter of Intent, parents can find valuable resources and templates to streamline the process, such as those available at homeschoolintent.com/editable-indiana-homeschool-letter-of-intent, which can assist in ensuring that all necessary information is accurately provided to the state.

Applications for Jobs - List any specific tools or equipment you have experience with.

| Fact Name | Details |

|---|---|

| Purpose | The TC-20 form is used by corporations in Utah to report franchise and income taxes for the tax year. |

| Filing Requirement | Corporations must file the TC-20 if they conduct any business activity in Utah during the taxable year. |

| Governing Law | The TC-20 form is governed by Utah Code §59-7, which outlines the tax obligations for corporations operating in the state. |

| Amended Returns | Corporations can file an amended return using the TC-20 form by marking the appropriate code if changes are needed after the initial submission. |

When filing the Utah TC-20 form, there are several other forms and documents that may be necessary to provide a complete picture of your corporation's tax situation. Understanding these additional documents can help ensure compliance and accuracy in your tax filings.

In summary, the Utah TC-20 form is often accompanied by several other schedules that provide necessary details for calculating taxable income and tax owed. By ensuring all related documents are completed and submitted, corporations can maintain compliance and potentially minimize their tax liabilities.

Filling out the Utah TC-20 form can be a daunting task, and many people make common mistakes that can lead to delays or complications. One frequent error is failing to indicate whether the corporation conducted any business activity in Utah during the taxable year. This is a crucial step, as it determines the corporation's tax obligations. If you forget to mark the appropriate box, it could result in penalties or an inaccurate tax assessment.

Another common mistake is neglecting to provide the correct Employer Identification Number (EIN). The EIN is essential for identifying the corporation and ensuring that all tax documents are correctly associated with it. If the EIN is incorrect or missing, it can lead to processing delays and potential issues with the IRS. Always double-check that the number you enter matches what the IRS has on file.

People also often miscalculate their total tax due. When completing the TC-20 form, ensure that you accurately subtract any refundable credits and prepayments from your total tax. If you make a mistake in these calculations, it could result in either underpayment or overpayment of taxes. Both scenarios can lead to additional complications, including interest and penalties.

Lastly, many individuals forget to sign the form or provide the preparer's information. The signature certifies that the information is true and complete to the best of your knowledge. Without it, the form may be considered incomplete. Additionally, if a preparer assists with the filing, their information must be included for any follow-up discussions with the Utah State Tax Commission. Omitting these details can lead to unnecessary delays in processing your return.

20201 |

|

|

|

|

Utah Corporation |

|

|

||||

|

|

|

|

Franchise and Income Tax Return |

|||||||

9998 |

|

|

|

|

|||||||

|

|

|

|

||||||||

|

|

|

|

For calendar year 2022 or fiscal year (mm/dd/yyyy): |

|||||||

|

|

|

|

||||||||

|

|

|

|

|

beginning - |

/ |

/ |

and ending - |

|||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

||||

|

|

• |

|

Amended Return (code |

• |

Mark “X” if you filed • |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

Corporation name |

|

|

|

|

|

federal form 8886 |

|||||

2022

/ /

Mark “X” for

Address |

|

|

|

|

Employer Identification Number |

|

|

|

|

|

|

|

|

City |

State |

|

ZIP + 4 |

|

UT Incorporation/Qualification No. |

|

|

|

|

|

|

|

|

Foreign country (if not U.S.) |

Telephone number |

|

|

|||

1 |

If this corporation conducted any Utah business activity during the taxable year, enter “X” |

• |

1 |

|

|

||||||

2 |

If this corporation joined in a federal consolidated return, enter “X” |

|

|

|

• |

2 |

|

|

|||

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

“water’s edge” |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

3 |

Mark “X” (one only) if this |

|

|

“water’s edge” |

|

|

election under |

|

|

|

“worldwide” |

|

return constitutes a: |

• 3a |

|

combined report |

• 3b |

|

UC |

• |

3c |

|

combined report |

|

|

|

|

|

|

|

|

|

|

|

|

4If this corporation made an election for any member of the federal affiliated group

|

during the taxable year, enter “X” |

|

|

|

|

IRC Section |

|

|

|

|

|

|

• 4a |

|

IRC Section 338 |

• 4b |

338(h)(10) |

• |

4c |

|

IRC Section 336(e) |

||

|

|

|

|

|

|

|

|

|

|

||

5 |

If this return includes any financial institution defined by Tax Commission Rule |

• |

5 |

|

|

||||||

6 |

Ultimate U.S. parent’s name |

|

|

|

|

|

EIN • |

6 |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

7 |

Total tax - enter amount from Schedule A, line 27 |

|

|

|

• |

7 |

|

|

|||

8 |

Total refundable credits and prepayments - enter amount from Schedule A, line 31 |

|

• |

8 |

|

|

|||||

|

|

|

|||||||||

9 |

Tax Due - subtract line 8 from line 7 (not less than zero) |

|

|

|

• |

9 |

|

|

|||

|

|

|

|

|

|||||||

10 |

Penalties and interest (see instructions) |

|

|

|

|

|

|

10 |

|

|

|

|

|

|

|

|

|

|

|

||||

11 |

Total Due - Pay this amount - add line 9 and line 10 |

|

|

|

• |

11 |

|

|

|||

|

|

|

|

|

|||||||

12 |

Overpayment - subtract the sum of line 7 and line 10 from line 8 (not less than zero) |

|

|

12 |

|

|

|||||

|

|

|

|

||||||||

13 |

Amount of overpayment on line 12 to be applied to next taxable year |

|

|

|

• |

13 |

|

|

|||

|

|

|

|

|

|||||||

14 |

Refund - subtract line 13 from line 12 |

|

|

|

|

|

• |

14 |

|

|

|

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

15 Mark “X” for each quarterly estimated prepayment |

• |

1st |

• |

2nd |

|

|

|

||||||||||

|

|

meeting an exception (attach documentation): |

|

|

|

|

|

|

|

|

|

USTC USE ONLY |

|||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

• |

3rd |

• |

4th |

|

|

|

||||||

|

|

|

|

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare to the best of my knowledge and belief, |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

this return and accompanying schedules are true, correct and complete. |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

SIGN |

Signature of officer |

Date |

|

Title |

|

|

|

“X” if USTC may discuss |

|||||||||

HERE |

|

|

|

|

|

|

|

|

|

|

this return with preparer below: |

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

Preparer’s signature |

Date |

|

Preparer’s telephone number |

Preparer’s |

PTIN |

||||||||

|

|

Paid |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

Preparer’s |

Firm’s name and address |

|

|

|

|

|

|

|

|

Preparer’s |

EIN |

|||||

|

Section |

|

|

|

|

|

|

|

|

|

|

• |

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Supplemental information to be Supplied by All Corporations |

Pg. 2 |

||||||||

20202 EIN |

|

|

|

|

|

2022 |

|

|

|

|

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

||

|

1 Date of incorporation: |

/ / |

|

State or country in which incorporated: |

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

mm/dd/yyyy

2If this corporation is dissolved or withdrawn, see Dissolution or Withdrawal in the General Instructions.

3If this corporation at any time during its tax year owned more than 50 percent of the voting stock of another corporation(s), provide the following for each corporation so owned. Attach additional pages if needed.

Name of corporation:

Address:

City, State, ZIP Code:

Percent of stock owned: |

% |

Date stock acquired: |

/ |

/ |

|

|

|

|

|

|

|

mm/dd/yyyy

4If more than 50 percent of the voting stock of this corporation is owned by another corporation, provide the following information about the other corporation.

Name of corporation:

Address:

City, State, ZIP Code:

Percent of stock owned: |

% |

|

|

|

|

5Check here if this corporation or its subsidiary(ies) had a change in control or ownership or acquired control or ownership of any other legal entity this year.

6Enter the location where the corporate books and records are maintained:

7Enter the state or country of commercial domicile:

• 8 Enter the |

/ |

/ |

|

|

|

mm/dd/yyyy

Under separate cover, send a summary and supporting schedules for all federal adjustments and the federal tax liability for each year for which federal audit adjustments have not been reported to the Tax Commission. Include the date of final determination. Send the information to:

Auditing Division, Utah State Tax Commission, 210 North 1950 West, Salt Lake City, UT

•9 Enter the

/ / |

/ / |

/ / |

/ / |

|||

|

|

|

|

|

|

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

•10 Enter the

/ / |

/ / |

/ / |

/ / |

|||

|

|

|

|

|

|

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

|

mm/dd/yyyy |

Note: Utah Code

|

|

Schedule A - Utah Net Taxable Income and Tax Calculation |

Pg. 1 |

||||||||||

20203 |

EIN |

|

|

|

|

|

|

2022 |

|

|

|

||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

|

||||

1 |

Unadjusted income/loss before NOL and special deductions from federal form 1120, line 28 |

• 1 |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

2 |

Additions to unadjusted income from Schedule B, line 19 |

|

|

• 2 |

|

|

|

||||||

3 |

Add line 1 and line 2 |

|

|

3 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

4 |

Subtractions from unadjusted income from Schedule C, line 21 |

|

|

• 4 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

5 |

Adjusted income/loss - subtract line 4 from line 3 |

|

|

• 5 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

6 |

Utah net nonbusiness income from Schedule H, line 14 |

|

|

• 6 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

7 |

|

|

• 7 |

|

|

|

|||||||

8 |

Total nonbusiness income net of expenses - add line 6 and line 7 |

|

|

8 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

||||||

9 |

Apportionable income/loss before contributions deduction - subtract line 8 from line 5 |

• 9 |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

10 |

Utah contributions deduction from Schedule D, line 6 |

|

|

• 10 |

|

|

|

||||||

11 |

Apportionable income/loss - subtract line 10 from line 9 |

|

|

11 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

12 |

Apportionment fraction - enter 1.000000, or Schedule J, line 9 or 10, if applicable |

12 |

|

|

|

|

|||||||

|

|

|

|

||||||||||

|

|

|

|

|

|

|

|

|

|||||

13 |

Apportioned income/loss - multiply line 11 by line 12 |

|

|

• 13 |

|

|

|

||||||

14 |

Utah net nonbusiness income (from line 6 above) |

|

|

14 |

|

|

|

|

|||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

15 |

Utah income/loss before Utah net loss deduction - add line 13 and line 14 |

|

|

• 15 |

|

|

|

||||||

|

|

|

|

|

|

|

|

||||||

16 |

Utah net loss carried forward from prior years (see instructions and attach documentation) |

• 16 |

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

17 |

Net Utah taxable income/loss - subtract line 16 from line 15 |

|

|

• 17 |

|

|

|

||||||

18 |

Calculation of tax (see instructions): |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|||||||

|

a Multiply line 17 by 4.85% (.0485) (not less than zero) |

18a |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

|

b Minimum tax - enter $100 or amount from Schedule M, line b |

• 18b |

|

|

|

|

|

||||||

|

Tax amount - enter the greater of line 18a or line 18b |

|

|

• 18 |

|

|

|

||||||

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|||||

19 |

Interest on installment sales |

|

|

• 19 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

20 |

IRC 965(a) deferred foreign income installment amount |

|

|

• 20 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

21 |

Recapture of |

|

|

• 21 |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|||||

22 |

Total tax - add lines 18 through 21 |

|

|

• 22 |

|

|

|

||||||

|

Carry to Schedule A, page 2, line 23 |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||

|

Schedule A - Utah Net Taxable Income and Tax Calculation |

Pg. 2 |

|||||||||||||||

20204 EIN |

|

|

|

|

|

|

|

|

|

|

2022 |

|

|

||||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

23 |

Enter tax from Schedule A, page 1, line 22 |

|

|

|

|

|

23 |

|

|

|

|||||||

24 |

Nonrefundable credits (see instructions or incometax.utah.gov/credits for codes) |

|

|

|

|

||||||||||||

|

|

|

|

||||||||||||||

|

|

|

Code |

Amount |

|

Code |

Amount |

|

|

|

|

||||||

|

• 24a |

|

|

|

|

• 24b |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• 24c |

|

|

|

|

• 24d |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• 24e |

|

|

|

|

• 24f |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Total nonrefundable credits - add lines 24a through 24f |

|

|

|

|

|

• 24 |

|

|

||||||||

|

|

|

|

|

|

||||||||||||

25 |

Net tax - subtract line 24 from line 23 (cannot be less than line 18b or less than zero) |

• 25 |

|

|

|||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

26 |

Utah use tax |

|

|

|

|

|

|

|

|

|

• 26 |

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

27 |

Total tax - add line 25 and line 26 |

|

|

|

|

|

• 27 |

|

|

||||||||

|

Enter here and on |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||||||||

28 |

Refundable credits (see instructions or incometax.utah.gov/credits for codes) |

|

|

|

|

|

|||||||||||

|

|

|

Code |

Amount |

|

Code |

Amount |

|

|

|

|

||||||

|

• 28a |

|

|

|

|

• 28b |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• 28c |

|

|

|

|

• 28d |

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Total refundable credits - add lines 28a through 28d |

|

|

|

|

|

• 28 |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

29 |

Prepayments from Schedule E, line 4 |

|

|

|

|

|

• 29 |

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||

30 |

Amended return only (see instructions) |

|

|

|

|

|

• 30 |

|

|

||||||||

|

|

|

|

|

|

|

|||||||||||

31 |

Total refundable credits and prepayments - add lines 28 through 30 |

|

• 31 |

|

|

||||||||||||

|

Enter here and on |

|

|

|

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

Schedule B - Additions to Unadjusted Income |

|||||||

20205 |

EIN |

|

|

2022 |

|

||||

USTC ORIGINAL FORM |

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

1 |

Interest from state obligations |

• 1 |

|||||||

|

|

|

|

|

|

|

|||

2 |

a Income taxes paid to any state |

• 2a |

|||||||

|

|

|

|

|

|||||

|

b Franchise or privilege taxes paid to any state |

• 2b |

|||||||

|

|

|

|

|

|||||

|

c Corporate stock taxes paid to any state |

• 2c |

|||||||

|

|

|

|

|

|||||

|

d Any income, franchise or capital stock taxes imposed by a foreign country |

• 2d |

|||||||

|

|

|

|

|

|||||

|

e Business and occupation taxes paid to any state |

• 2e |

|||||||

|

|

|

|

|

|||||

3 |

Safe harbor lease adjustments |

• 3 |

|||||||

|

|

|

|

|

|||||

4 |

Capital loss carryover |

• 4 |

|||||||

|

|

|

|

|

|||||

5 |

Federal deductions taken previously on a Utah return |

• 5 |

|||||||

|

|

|

|

|

|||||

6 |

Federal charitable contributions from federal form 1120, line 19 |

• 6 |

|||||||

|

|

|

|

|

|||||

7 |

Gain/loss on IRC Sections 338(h)(10) or 336(e) |

• 7 |

|||||||

|

|

|

|

|

|||||

8 |

Adjustments due to basis difference |

• 8 |

|||||||

|

|

|

|

|

|||||

9 |

Expenses attributable to 50 percent unitary foreign dividend exclusion |

• 9 |

|||||||

|

|

|

|

|

|||||

10 |

Installment sales income previously reported for federal but not Utah purposes |

• 10 |

|||||||

|

|

|

|

|

|||||

11 |

Nonqualified withdrawal from my529 |

• 11 |

|||||||

|

|

|

|

|

|||||

12 |

Income/loss from IRC Section 936 corporations |

• 12 |

|||||||

|

|

|

|

|

|||||

13 |

Foreign income/loss for worldwide combined filers |

• 13 |

|||||||

|

|

|

|

|

|||||

14 |

Income/loss of unitary corporations not included in federal consolidated return |

• 14 |

|||||||

|

|

|

|

|

|||||

15 |

Deductions for a royalty or other expense paid to an entity related by common ownership (see instructions) |

• 15 |

|||||||

|

|

|

|

|

|||||

16 |

Payroll Protection Program grant or loan addback (see instructions) |

• 16 |

|||||||

|

|

|

|

|

|||||

17 |

(Reserved, see instructions) |

• 17 |

|||||||

|

|

|

|

|

|||||

18 |

(Reserved, see instructions) |

• 18 |

|||||||

|

|

|

|

|

|||||

19 |

Total additions - add lines 1 through 18 |

• 19 |

|||||||

|

Enter here and on Schedule A, line 2 |

|

|

|

|||||

|

|

|

|

||||||

Schedule C - Subtractions from Unadjusted Income

20206 EIN

USTC ORIGINAL FORM

1Intercompany dividend elimination (see instructions)

2 Foreign dividend

3 Net capital loss

4a Federal jobs credit salary reduction

b Federal research and development credit expense reduction

c Federal orphan drug credit clinical testing expense reduction

d Expense reduction for other federal credits (attach schedule)

e.Federal qualified tax credit bond credit, income increase

f.Federal qualified zone academy bond credit, income increase

5 Safe harbor lease adjustments

6 Federal income previously taxed by Utah

7 Fifty percent exclusion for dividends from unitary foreign subsidiaries

8 Fifty percent exclusion for foreign operating company income/loss

9Gain/loss on stock sale not recognized for federal purposes (but included in taxable income) when IRC Section 338(h)(10) or 336(e) has been elected

10Basis adjustments

11Interest expense not deducted on federal return under IRC Section 265(b) or 291(e)

12Dividends received from admitted insurance company subsidiaries exempt under UC

13Contributions to my529 account(s)

14(Reserved, see instructions)

15Dividends received or deemed received by a member of the unitary group from a captive REIT

16IRC Section 857(b)(2)(E) deduction from a captive REIT

17FDIC Premiums disallowed as a deduction for federal income tax purposes

18

19(Reserved, see instructions)

20(Reserved, see instructions)

21Total subtractions - add lines 1 through 20

Enter here and on Schedule A, line 4

•1

•2

•3

•4a

•4b

•4c

•4d

•4e

•4f

•5

•6

•7

•8

•9

•10

•11

•12

•13

•14

•15

•16

•17

•18

•19

•20

•21

|

Schedule D - Utah Contributions Deduction |

|

|

||||||

20207 EIN |

|

|

2022 |

|

|

||||

USTC ORIGINAL FORM |

|

|

|

|

|

|

|||

1 |

Apportionable income before contributions deduction from Schedule A, line 9 |

|

|

• 1 |

|||||

|

If a loss, no contribution deduction is allowed |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

2 |

Utah contribution limitation - multiply line 1 by 10% (.10) (not less than zero) |

2 |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

3 |

Current year contributions |

|

|

• 3 |

|||||

|

|

|

|

|

|

|

|

||

4 |

Utah contributions carryforward (attach schedule) |

|

|

• 4 |

|||||

5 |

Total contributions available - add line 3 and line 4 |

5 |

|

|

|

||||

|

|

|

|||||||

|

|

|

|

|

|

|

|

||

6 |

Utah contributions deduction - lesser of line 2 or line 5 |

|

|

• 6 |

|||||

|

Enter here and on Schedule A, line 10 |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|||

7 |

Contribution carryover to next year - subtract line 6 from line 5 |

• 7 |

|||||||

|

|

|

|

|

|

|

|

|

|

|

Schedule E - Prepayments of Any Type |

|

||||

1 |

Overpayment applied from prior year |

|

|

1 |

|

|

2 |

Extension prepayment |

Date: |

/ / |

Check no.: |

2 |

|

|

||||||

Enter the date and amount of any extension prepayment. If paid by check, enter the check number.

3Other prepayments (attach additional pages if necessary)

Enter the date and amount of any prepayment for the filing period. If paid by check, enter the check number.

a Date: |

/ |

/ |

Check no.: |

|

3a |

|

|

|

|

|

|

b Date: |

/ |

/ |

Check no.: |

|

3b |

|

|

|

|

|

|

c Date: |

/ |

/ |

Check no.: |

|

3c |

|

|

|

|

|

|

d Date: |

/ |

/ |

Check no.: |

|

3d |

|

|

|

|

|

|

Total of all prepayments - add lines 3a through 3d |

3 |

4 Total prepayments - add lines 1 through 3 |

4 |

Enter here and on Schedule A, line 29 |

|

Schedule H - Utah Nonbusiness Income Net of Expenses |

Pg. 1 |

|||||

20261 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Failure to complete this form may result in disallowance of the nonbusiness income. |

|

|

|

|

|||||||

Part 1 - Utah Nonbusiness Income (nonbusiness income allocated to Utah) |

|

|

|

|

|||||||

|

|

|

|

||||||||

|

|

|

|

||||||||

|

A |

B |

|

|

C |

D |

|

E |

|||

|

Type of Utah |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

Utah Nonbusiness Income |

||||

|

Nonbusiness Income |

Utah Nonbusiness |

|

Used to Produce Utah |

Used to Produce Utah |

|

|

|

|||

|

|

|

Asset(s) |

|

|

Nonbusiness Income |

Nonbusiness Income |

|

|

|

|

1a |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1b |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1c |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1d |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1e |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

2Total of column C and column D

3Total Utah nonbusiness income - add column E for lines 1a through 1e

|

Description of direct expenses related to: |

Amount of Direct Expense |

||

4a |

Line 1a above |

|

||

|

|

|

|

|

4b |

Line 1b above |

|

||

|

|

|

|

|

4c |

Line 1c above |

|

||

|

|

|

|

|

4d |

Line 1d above |

|

||

|

|

|

|

|

4e |

Line 1e above |

|

||

|

|

|

|

|

5Total direct related expenses - add lines 4a through 4e

6 |

Utah nonbusiness income net of direct related expenses - subtract line 5 from line 3 |

|

• |

||

|

|

Column A |

Column B |

||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

||

|

Utah Nonbusiness Income |

Utah Nonbusiness Income |

|

|

|

7 |

|

|

|

|

|

|

(enter in Column A the amount from line 2, col. C) |

|

|

|

|

|

|

|

|

|

|

8

(enter in Column A the amount from line 2, col. D)

9Sum of beginning and ending asset values (add line 7 and line 8)

10Average asset value - divide line 9 by 2

11Utah nonbusiness assets ratio - line 10, Column A, divided by line 10, Column B (to four decimal places)

12Interest expense deducted in computing Utah taxable income (see instructions)

13Indirect related expenses for Utah nonbusiness income - multiply line 11 by line 12

14 Total Utah nonbusiness income net of expenses - subtract line 13 from line 6 |

|

• |

|

Enter on: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule H - |

Pg. 2 |

|||||

20262 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Part 2 -

|

A |

B |

|

|

C |

D |

|

E |

||

|

Type of |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

||||

|

Nonbusiness Income |

|

|

Used to Produce |

Used to Produce |

|

Income |

|||

|

|

|

Nonbusiness Asset(s) |

|

Nonbusiness Income |

Nonbusiness Income |

|

|

||

15a |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15b |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15c |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15d |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15e |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

16Total of column C and column D

17Total

|

Description of direct expenses related to: |

|

|

|

|

|

Amount of Direct Expense |

|

18a |

Line 15a above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18b |

Line 15b above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18c |

Line 15c above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18d |

Line 15d above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18e |

Line 15e above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

Total direct related expenses - add lines 18a through 18e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

20 |

• |

|||||||

|

|

|

Column A |

Column B |

|

|

||

|

|

|

|

|

||||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

|

|

|||

|

|

|

|

|

||||

21 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. C) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

22 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

23Sum of beginning and ending asset values (add line 21 and line 22)

24Average asset value - divide line 23 by 2

25

26Interest expense deducted in computing

27Indirect related expenses for

28 Total |

• |

|

Enter on: |

|

|

|

|

|

|

|

|

Schedule J - Apportionment Schedule |

Pg. 1 |

|||||

20263 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Use this schedule only if the entity does business in Utah and one or more other states and income must be apportioned to Utah.

Briefly describe the nature and location(s) of your Utah business activities:

Apportionable Income Factors

|

|

|

|

|

Column A |

|

Column B |

|||

1 |

Property Factor |

|

|

Inside Utah |

|

Inside and Outside Utah |

||||

|

a |

Land |

• 1a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

b |

Depreciable assets |

• 1b |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Inventory and supplies |

• 1c |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Rented property |

• 1d |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Other allowable property (see instructions) |

• 1e |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

f |

Total tangible property - add lines 1a through 1e |

• 1f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

2 |

Property factor - divide line 1f, Column A, by line 1f, Column B (to six decimal places) |

• |

2 |

|

|

|

||||

3 |

Payroll Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total wages, salaries, commissions and other compensation |

• 3a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

4 |

Payroll factor - divide line 3a, Column A, by line 3a, Column B (to six decimal places) |

• |

4 |

|

|

|

||||

5 |

Sales Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total sales (gross receipts less returns and allowances) |

|

|

|

• |

5a |

|||

|

b |

Sales delivered or shipped to Utah buyers from outside Utah |

• 5b |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Sales delivered or shipped to Utah buyers from within Utah |

• 5c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Sales shipped from Utah to the United States government |

• 5d |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Sales shipped from Utah to buyers in states where the corp. |

• 5e |

|

|

|

|

|

||

|

|

has no nexus (corporation not taxable in buyer’s state) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f |

Rent and royalty income |

• 5f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

g |

Services and other allowable sales (see instructions) |

• 5g |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

h |

Total sales (add lines 5a through 5g) |

• 5h |

• |

|

|

|

|

||

|

|

|

|

|

|

|

||||

6 Sales factor - line 5h, Column A, divided by line 5h, Column B (to six decimals) |

• |

6 |

|

|

|

|||||

|

|

Continued on page 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

When filling out the Utah TC-20 form, there are several important points to keep in mind to ensure accuracy and compliance.