Blank Utah Tc 40V Form

Blank Utah Tc 40V Form

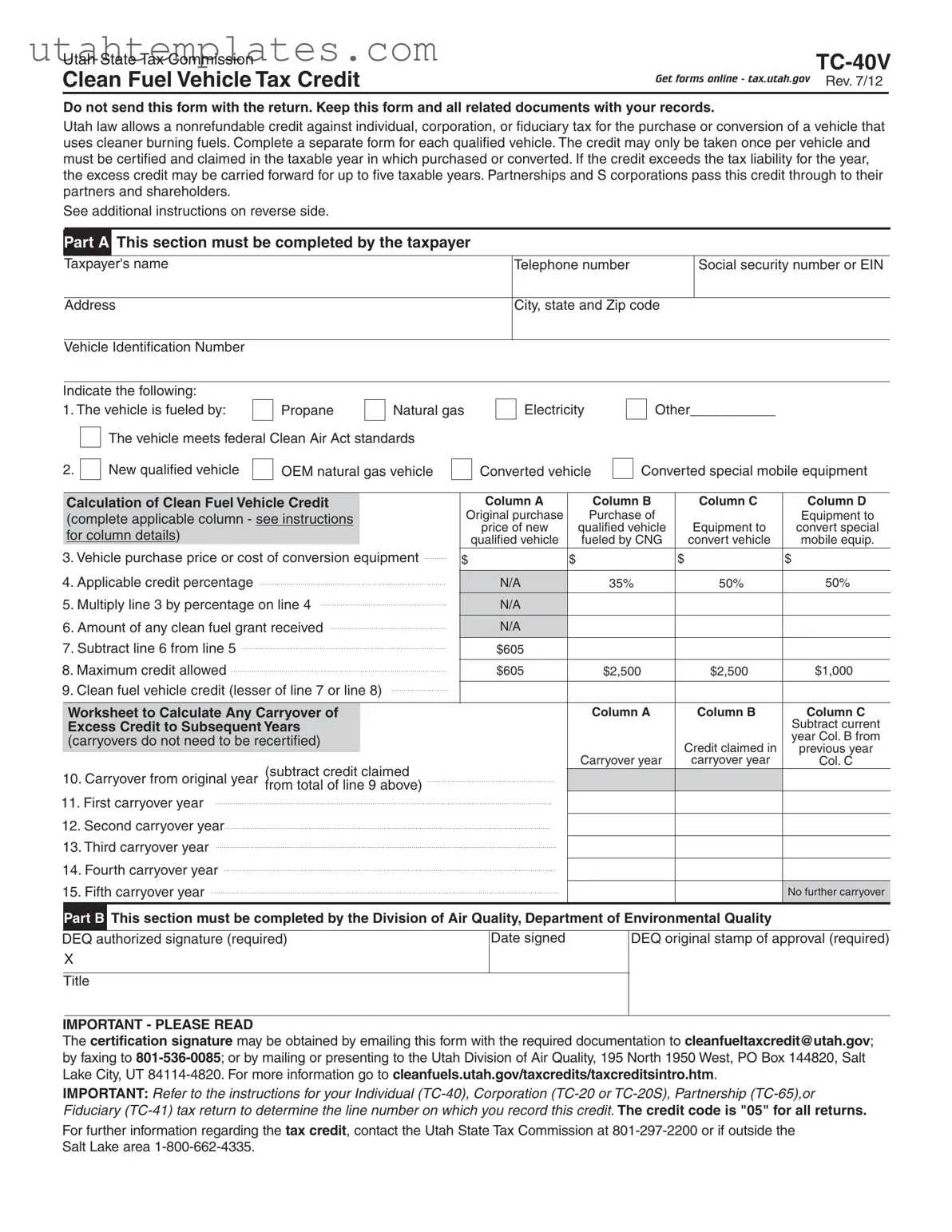

The Utah TC-40V form plays a vital role in promoting the use of clean fuel vehicles by offering tax credits to individuals and businesses that invest in environmentally friendly transportation options. This form allows taxpayers to claim a nonrefundable credit against various taxes for the purchase or conversion of vehicles that utilize cleaner burning fuels such as propane, natural gas, or electricity. Each qualified vehicle requires a separate form, and the credit can only be claimed once per vehicle, ensuring that the incentive is both effective and manageable. Taxpayers must complete the form in the taxable year of the vehicle's purchase or conversion, and if the credit exceeds their tax liability, they can carry forward the excess for up to five years. The TC-40V form includes sections for personal information, vehicle details, and calculations related to the credit amount, which varies depending on the type of vehicle and the nature of the conversion. Additionally, the form requires certification from the Utah Division of Air Quality, ensuring that all vehicles meet specific environmental standards. By understanding the nuances of the TC-40V, taxpayers can effectively navigate the process and take advantage of this opportunity to contribute to a cleaner environment while also benefiting financially.

Utah 3045 - It includes a description of the property connected to the security instrument.

To effectively initiate the homeschooling journey in Indiana, families must familiarize themselves with the essential components of the process, particularly the Indiana Homeschool Letter of Intent, which can be found at homeschoolintent.com/editable-indiana-homeschool-letter-of-intent/. This form not only serves as a formal notification to the state but also ensures that families adhere to the necessary regulations, paving the way for a smooth educational transition.

Car Gift - Changes to authorized individuals must be communicated promptly.

What Is Dopl - The applicant must provide their name and the name of the franchise they represent on the form.

| Fact Name | Description |

|---|---|

| Form Purpose | The TC-40V form is used to claim the Clean Fuel Vehicle Tax Credit in Utah. |

| Governing Law | This form is governed by Utah Code sections 59-7-605 and 59-10-1009. |

| Nonrefundable Credit | The credit is nonrefundable, meaning it can only reduce tax liability to zero but not result in a refund. |

| One Credit Per Vehicle | A taxpayer can claim the credit only once for each qualified vehicle. |

| Carryforward Option | If the credit exceeds the tax liability, the excess can be carried forward for up to five years. |

| Certification Requirement | The credit must be certified and claimed in the taxable year when the vehicle is purchased or converted. |

| Qualified Vehicles | Vehicles must use cleaner-burning fuels, such as propane or natural gas, to qualify for the credit. |

| Documentation | Taxpayers should keep the TC-40V form and all related documents for their records, but do not send it with the tax return. |

| Credit Amounts | The maximum credit amounts vary: $605 for new vehicles, $2,500 for OEM CNG vehicles, and $1,000 for special mobile equipment. |

| Contact Information | For questions, taxpayers can contact the Utah State Tax Commission at 801-297-2200 or 1-800-662-4335 for those outside Salt Lake City. |

The Utah TC-40V form is essential for claiming the Clean Fuel Vehicle Tax Credit. However, several other forms and documents are often used alongside it to ensure compliance and proper processing. Below is a list of these important documents.

It is important to keep all related documents organized and accessible. This ensures that you can provide the necessary information when claiming your tax credits. Proper documentation helps streamline the process and avoid any potential issues with your tax filings.

Filling out the Utah TC-40V form can be a straightforward process, but there are common mistakes that can lead to complications. One frequent error is failing to complete all required sections. Each part of the form serves a specific purpose, and omitting even one detail can result in delays or rejections. Ensure that every section, particularly the taxpayer's information and vehicle details, is filled out completely.

Another mistake is not providing the correct Vehicle Identification Number (VIN). This number is crucial for identifying the vehicle and ensuring that it qualifies for the tax credit. Double-check the VIN against your vehicle's title or registration documents. Any discrepancies can cause issues when processing your claim.

Many people also overlook the importance of accurate calculations. In Part A, calculations must be precise, especially when determining the clean fuel vehicle credit. Errors in math can lead to claiming an incorrect amount, which may necessitate further clarification or correction with the tax authority.

Some taxpayers mistakenly believe they can submit the TC-40V form with their tax return. This is not the case. It is essential to keep the TC-40V form and all related documents for your records, but do not send it with your tax return. This misunderstanding can cause unnecessary confusion and delays in processing your tax credit.

Additionally, failing to obtain the necessary certification from the Utah Division of Air Quality is a common pitfall. The credit is not valid without an authorized signature and certification stamp. Ensure you follow the procedures for obtaining this certification before submitting your form.

Another error involves misunderstanding the credit limits based on the vehicle type. Each category—new qualified vehicles, OEM vehicles fueled by compressed natural gas, and conversion equipment—has different maximum credit amounts. Be sure to reference the specific limits for your situation to avoid claiming more than allowed.

Lastly, many taxpayers forget to keep a copy of the TC-40V form and related documents. This documentation is vital for your records and may be needed for future reference, especially if you decide to carry over any unused credits. Keeping thorough records can save you time and stress down the road.

Utah State Tax Commission |

|

||

Clean Fuel Vehicle Tax Credit |

Get forms online - tax.utah.gov |

Rev. 7/12 |

|

|

|

|

|

Do not send this form with the return. Keep this form and all related documents with your records.

Utah law allows a nonrefundable credit against individual, corporation, or fiduciary tax for the purchase or conversion of a vehicle that uses cleaner burning fuels. Complete a separate form for each qualified vehicle. The credit may only be taken once per vehicle and must be certified and claimed in the taxable year in which purchased or converted. If the credit exceeds the tax liability for the year, the excess credit may be carried forward for up to five taxable years. Partnerships and S corporations pass this credit through to their partners and shareholders.

See additional instructions on reverse side.

Part A This section must be completed by the taxpayer

Taxpayer's name

Telephone number

Social security number or EIN

Address

City, state and Zip code

Vehicle Identification Number

Indicate the following: |

|

|

1. The vehicle is fueled by: |

Propane |

Natural gas |

The vehicle meets federal Clean Air Act standards

Electricity

Other___________

2.

New qualified vehicle

OEM natural gas vehicle

Converted vehicle

Converted special mobile equipment

|

Calculation of Clean Fuel Vehicle Credit |

|

Column A |

Column B |

Column C |

Column D |

|

(complete applicable column - see instructions |

|

Original purchase |

Purchase of |

Equipment to |

Equipment to |

|

|

price of new |

qualified vehicle |

convert special |

||

|

for column details) |

|

||||

|

|

qualified vehicle |

fueled by CNG |

convert vehicle |

mobile equip. |

|

3. Vehicle purchase price or cost of conversion equipment |

|

|

|

|

||

$ |

$ |

$ |

$ |

|||

4. Applicable credit percentage |

|

|

|

|

||

N/A |

35% |

50% |

50% |

|||

5. Multiply line 3 by percentage on line 4 |

N/A |

|

|

|

||

6. Amount of any clean fuel grant received |

N/A |

|

|

|

||

7. Subtract line 6 from line 5 |

$605 |

|

|

|

||

8. Maximum credit allowed |

|

|

|

|

||

$605 |

$2,500 |

$2,500 |

$1,000 |

|||

9. Clean fuel vehicle credit (lesser of line 7 or line 8) |

|

|

|

|

||

|

|

|

|

|||

|

|

|

|

|

|

|

|

Worksheet to Calculate Any Carryover of |

|

|

Column A |

Column B |

Column C |

|

Excess Credit to Subsequent Years |

|

|

|

|

Subtract current |

|

(carryovers do not need to be recertified) |

|

|

|

Credit claimed in |

year Col. B from |

|

|

|

|

previous year |

||

|

|

|

|

|

||

|

(subtract credit claimed |

|

Carryover year |

carryover year |

Col. C |

|

|

|

|

|

|

||

10. Carryover from original year from total of line 9 above) |

|

|

|

|

||

11. First carryover year |

|

|

|

|

||

12. Second carryover year |

|

|

|

|

||

|

|

|

|

|||

13. Third carryover year |

|

|

|

|

||

|

|

|

|

|||

14. Fourth carryover year |

|

|

|

|

||

|

|

|

|

|||

15. Fifth carryover year |

|

|

|

|

||

|

|

|

No further carryover |

|||

|

|

|

|

|

|

|

Part B This section must be completed by the Division of Air Quality, Department of Environmental Quality

DEQ authorized signature (required) |

Date signed |

X

Title

DEQ original stamp of approval (required)

IMPORTANT - PLEASE READ

The certification signature may be obtained by emailing this form with the required documentation to cleanfueltaxcredit@utah.gov; by faxing to

IMPORTANT: Refer to the instructions for your Individual

For further information regarding the tax credit, contact the Utah State Tax Commission at

Instructions for the Clean Fuel Vehicle Tax Credit -

Taxpayers may claim a nonrefundable tax credit against Utah individual income tax, corporate franchise tax or fiduciary tax. (See Utah Code sections

The credit may only be taken once per vehicle. It must be certified and claimed in the taxable year in which the item is purchased or converted.

Column A - New Vehicle Meeting Air Quality and Fuel Economy Standards for Combined City and Highway, and Not Fueled by Compressed Natural Gas

A qualified vehicle is an original purchase, registered and titled for the first time in Utah, and having less than 7,500 miles. The vehicle must be certified by the Utah Department of Environmental Quality and meet both of the following standards:

1.Fuel Economy Standards for Combined City and Highway

a.at least 31 miles per gallon for

b.at least 36 miles per gallon for

c.at least 19 miles per gallon for vehicles fueled by a blend of 85% ethanol and 15% gasoline;

d.at least 19 miles per gallon for liquified petroleum

e.meet standards consistent with 40 C.F.R.

2.Air quality standards which are equal to or cleaner than the standards established in bin 2 in Table

The credit amount is $605.

Column B - OEM Vehicle Fueled by Compressed Natural Gas

A qualified vehicle is one fueled by compressed natural gas, and is registered in Utah.

The credit is the lesser of 35% of the purchase price of the vehicle less any clean fuel grant received, or $2,500.

Column C - Equipment to Convert Vehicle to Run on Propane, Natural Gas, Electricity, or Other Approved Fuel

A qualified vehicle must be registered in Utah and meet one of the following conditions:

1.It converts the engine to be fueled by propane, compressed natural gas, or electricity;

2.It converts the engine to be fueled by another fuel determined by the Air Quality Board to be as effective as the above listed fuels, or

3.It converts the vehicle to meet the

The credit is the lesser of 50% of the cost of the conversion equipment less any clean fuel grant received, or $2,500.

Column D - Equipment to Convert Special Mobile Engine to Operate on Propane, Natural Gas, Electricity, or Other Approved Fuel

A qualified vehicle must meet one of the following conditions:

1.It converts the engine to be fueled by propane, compressed natural gas, or electricity;

2.It converts the engine to be fueled by another fuel determined by the Air Quality Board to be as effective as the above listed fuels, or

3.It converts the engine to be substantially more effective in reducing air pollution than the fuel for which the engine was originally designed.

The credit is the lesser of 50% of the cost of the conversion equipment less any clean fuel grant received, or $1,000.

Procedures

1.If you have purchased a qualifying vehicle or converted a vehicle or special mobile equipment engine, submit the required documentation with a completed form

2.The taxpayer must receive certification from the Utah Division of Air Quality. The credit is not valid unless both an authorized signature and certification stamp are present.

3.Complete the calculation of the credit in Part A. Carryover credits may be recorded on lines 10 through 15. Carryover credits do not need to be recertified by the Utah Division of Air Quality.

4.Refer to the return instructions to determine the line number on which to record this credit. The credit code is "05" for all returns.

5.Do not send this form with your return. Keep this form and all related documents with your records.

The Utah TC-40V form is designed for taxpayers seeking a tax credit for clean fuel vehicles. Several other documents serve similar purposes in various contexts. Here are eight documents that share similarities with the TC-40V form:

Each of these forms serves to promote cleaner vehicle technologies and reduce environmental impact, reflecting a broader commitment to sustainability across various states.

Filling out the Utah TC-40V form can be a straightforward process if you keep a few key points in mind. Here are some essential takeaways to help you navigate the form effectively:

By keeping these points in mind, you can ensure a smoother experience when filling out and using the Utah TC-40V form. Understanding the requirements and procedures will help you maximize your tax benefits while staying compliant with state regulations.