Blank Utah Tc 41 Form

Blank Utah Tc 41 Form

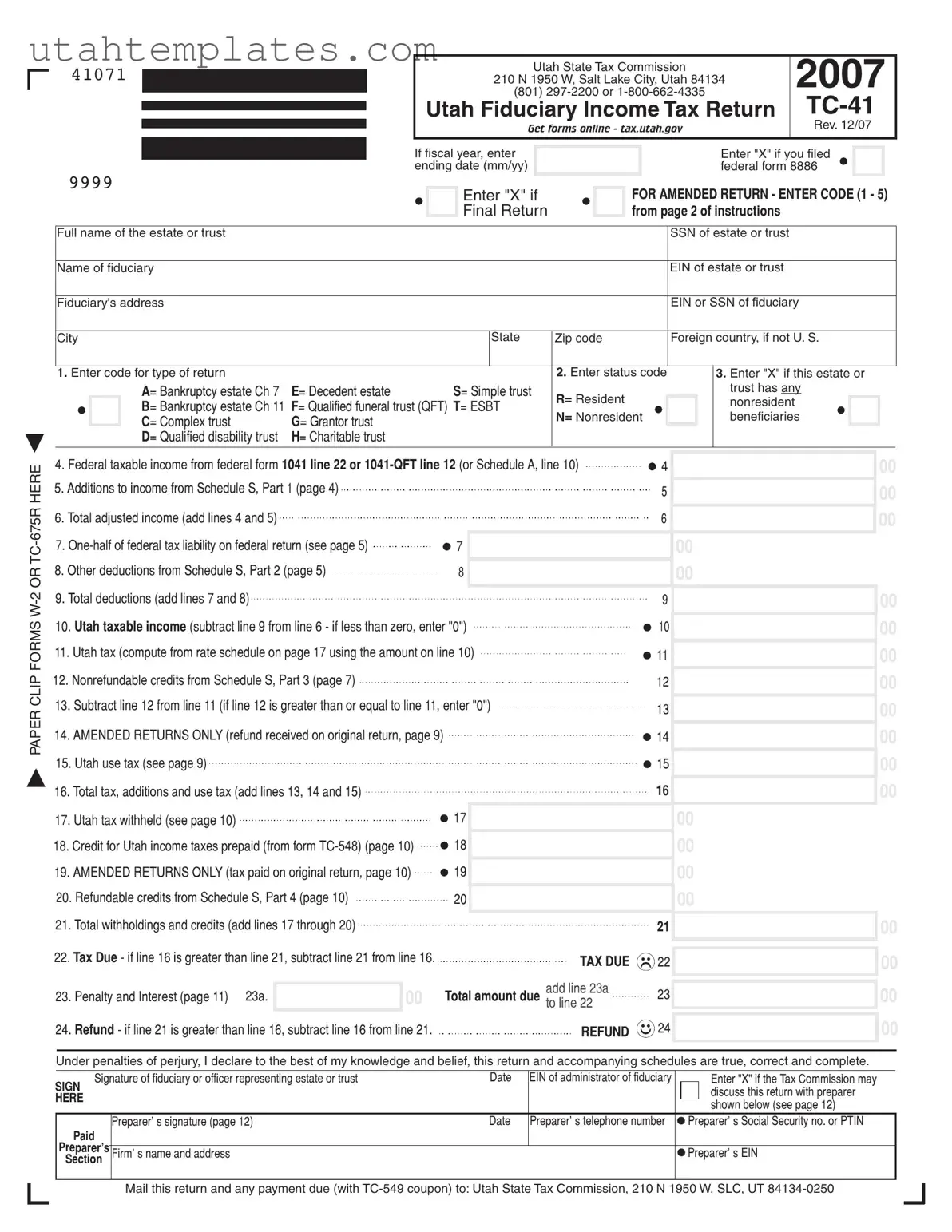

The Utah TC-41 form is an essential document for fiduciaries managing estates and trusts within the state. This form serves as the Utah Fiduciary Income Tax Return, allowing fiduciaries to report income, deductions, and tax liabilities for estates and trusts. When completing the TC-41, fiduciaries must provide key information such as the estate or trust's name, its Social Security Number (SSN) or Employer Identification Number (EIN), and the fiduciary's details. The form includes various sections to calculate federal taxable income, adjustments, and applicable deductions. Additionally, it addresses specific scenarios, such as amended returns and the presence of nonresident beneficiaries. Understanding the nuances of the TC-41 is crucial, as it directly impacts the tax obligations of estates and trusts, ensuring compliance with Utah tax regulations while maximizing potential credits and deductions. By navigating this form accurately, fiduciaries can fulfill their responsibilities effectively and avoid pitfalls that may arise during the tax filing process.

Utah Tc-40 Instructions - Record the patient's age accurately on the form.

For those in need of a reliable method to document the sale, our all-inclusive guide on how to complete a Trailer Bill of Sale is essential. This form not only serves as proof of ownership transfer but also ensures all necessary details are accurately recorded during the transaction. Visit our resource for the Trailer Bill of Sale process to access and fill out your form seamlessly.

Applications for Jobs - Disclose if you have previously applied to this company, if so, when and where.

| Fact Name | Details |

|---|---|

| Form Purpose | The TC-41 form is used for filing the Utah Fiduciary Income Tax Return. |

| Governing Law | This form is governed by the Utah State Tax Code, Title 59. |

| Filing Deadline | The TC-41 must be filed by the 15th day of the fourth month following the end of the tax year. |

| Amended Returns | If you need to amend a return, enter an "X" in the designated box and provide the appropriate code. |

| Tax Calculation | Utah tax is computed based on the taxable income reported on line 10 of the form. |

| Refunds | If the total withholdings exceed the tax due, a refund will be issued to the fiduciary. |

| Contact Information | For assistance, contact the Utah State Tax Commission at (801) 297-2200 or 1-800-662-4335. |

| Filing Location | Mail the completed TC-41 to the Utah State Tax Commission at 210 N 1950 W, Salt Lake City, UT 84134-0250. |

The Utah TC-41 form is essential for filing fiduciary income tax returns in the state of Utah. Several other forms and documents are often used in conjunction with the TC-41 to ensure accurate reporting and compliance. Below is a list of these forms, each with a brief description.

Using these forms alongside the TC-41 will help ensure a smooth filing process and compliance with Utah tax regulations. Always double-check each document for accuracy and completeness to avoid any issues with the tax authorities.

Completing the Utah TC-41 form can be a complex process, and mistakes can lead to delays or issues with tax filings. One common error occurs when individuals fail to provide the correct federal taxable income. This information must be accurately transferred from federal form 1041, line 22, or 1041-QFT, line 12. Omitting or misreporting this figure can significantly affect the calculations that follow.

Another frequent mistake is neglecting to check the appropriate boxes for the type of return being filed. The form includes various codes for different types of estates and trusts, such as bankruptcy estates or charitable trusts. Failing to mark the correct code can result in the form being processed incorrectly, potentially leading to unnecessary complications.

Many filers also overlook the requirement to attach necessary documents, such as Forms W-2 or TC-675R. These forms must be paper-clipped to the TC-41 to substantiate the income reported. Without these attachments, the tax commission may reject the return or request additional information, prolonging the process.

Inaccurate calculations are another common issue. Individuals may miscalculate total adjusted income by incorrectly adding or subtracting figures from previous lines. It is essential to double-check all arithmetic to ensure that the final amounts are correct. Mistakes in calculations can lead to incorrect tax due or refunds, which can complicate future filings.

Furthermore, some people forget to include their signature and date on the form. This step is crucial, as the tax commission requires a signed declaration affirming the accuracy of the information provided. An unsigned form will be considered incomplete and may delay processing.

Another common oversight is failing to enter the Employer Identification Number (EIN) or Social Security Number (SSN) of the fiduciary. This identification is necessary for the tax commission to process the return correctly. Incomplete identification can lead to complications in tracking the return and any associated payments.

When it comes to claiming credits, some filers may not fully understand the requirements for nonrefundable and refundable credits. Misreporting these credits can lead to discrepancies in the final tax amount owed or refunded. It is important to carefully review the instructions and ensure all applicable credits are claimed accurately.

Lastly, individuals sometimes neglect to keep copies of their completed forms and any supporting documentation. Maintaining records of submitted forms is essential for future reference and in case of audits or inquiries from the tax commission. Keeping a well-organized file can save time and stress later on.

|

|

|

|

|

|

|

|

|

(801) |

|

|

2007 |

||||||||||

41071 |

|

|

|

|

|

|

Utah State Tax Commission |

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

210 N 1950 W, Salt Lake City, Utah 84134 |

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

Utah Fiduciary Income Tax Return |

|

|

||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

Get forms online - tax.utah.gov |

|

|

|

Rev. 12/07 |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

|

|

|

|

|

If fiscal year, enter |

|

|

|

|

|

|

|

Enter "X" if you filed |

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

|

|

|

|

|

|

ending date (mm/yy) |

|

|

|

|

|

|

|

federal form 8886 |

|

|

||||||

9999 |

|

|

|

|

|

|

Enter "X" if |

|

|

FOR AMENDED RETURN - ENTER CODE (1 - 5) |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|||||||||||||

|

|

|

|

|

|

|

|

Final Return |

|

|

from page 2 of instructions |

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Full name of the estate or trust |

|

|

|

|

|

|

|

|

|

|

|

SSN of estate or trust |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Name of fiduciary |

|

|

|

|

|

|

|

|

|

|

|

EIN of estate or trust |

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

Fiduciary's address |

|

|

|

|

|

|

|

|

|

|

|

EIN or SSN of fiduciary |

|

|

|

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

City |

|

|

|

|

|

State |

Zip code |

|

|

Foreign country, if not U. S. |

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

1. Enter code for type of return |

|

|

|

|

|

|

|

2. Enter status code |

3. Enter "X" if this estate or |

|||||||||||||

|

|

A= Bankruptcy estate Ch 7 |

E= Decedent estate |

|

S= Simple trust |

R= Resident |

|

|

|

|

trust has any |

|

|

|

||||||||

|

|

B= Bankruptcy estate Ch 11 |

F= Qualified funeral trust (QFT) T= ESBT |

|

|

|

|

nonresident |

|

|

|

|

||||||||||

|

|

N= Nonresident |

|

|

beneficiaries |

|

|

|

||||||||||||||

|

|

C= Complex trust |

G= Grantor trust |

|

|

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

|

D= Qualified disability trust |

H= Charitable trust |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PAPER CLIP FORMS

4. Federal taxable income from federal form 1041 line 22 or |

4 |

|

||||

5. Additions to income from Schedule S, Part 1 (page 4) |

|

|

|

5 |

|

|

|

|

|

|

|

|

|

6. Total adjusted income (add lines 4 and 5) |

|

|

|

6 |

|

|

|

|

|

|

|||

|

|

|

|

|||

7. |

|

7 |

|

|

|

|

|

|

|

|

|||

8. Other deductions from Schedule S, Part 2 (page 5) |

|

8 |

|

|

|

|

|

|

|

|

|||

9. Total deductions (add lines 7 and 8) |

|

|

|

|

|

|

|

|

|

9 |

|

||

|

|

|

|

|||

10. Utah taxable income (subtract line 9 from line 6 - if less than zero, enter "0") |

10 |

|

||||

|

||||||

11. Utah tax (compute from rate schedule on page 17 using the amount on line 10) |

11 |

|

||||

12. Nonrefundable credits from Schedule S, Part 3 (page 7) |

|

|

|

12 |

|

|

13. Subtract line 12 from line 11 (if line 12 is greater than or equal to line 11, enter "0") |

13 |

|

||||

|

|

|

|

|

|

|

14. AMENDED RETURNS ONLY (refund received on original return, page 9) |

|

|

14 |

|

||

15. Utah use tax (see page 9) |

|

|

|

15 |

|

|

16. Total tax, additions and use tax (add lines 13, 14 and 15) |

|

|

|

16 |

|

|

|

|

|

|

|||

17. Utah tax withheld (see page 10) |

|

17 |

|

|

|

|

18. Credit for Utah income taxes prepaid (from form |

18 |

|

|

|

||

19. AMENDED RETURNS ONLY (tax paid on original return, page 10) |

19 |

|

|

|

||

|

|

|

||||

20. Refundable credits from Schedule S, Part 4 (page 10) |

|

20 |

|

|

|

|

|

|

|

|

|||

21. Total withholdings and credits (add lines 17 through 20) |

|

|

|

|

|

|

|

|

|

21 |

|

||

22. Tax Due - if line 16 is greater than line 21, subtract line 21 from line 16. |

|

TAX DUE |

22 |

|

||

|

|

|||||

|

|

|

|

|

||

|

|

00 |

|

add line 23a |

23 |

|

|

|

|

|

|||

23. Penalty and Interest (page 11) 23a. |

|

Total amount due to line 22 |

|

|||

|

|

|

||||

24. Refund - if line 21 is greater than line 16, subtract line 16 from line 21. |

|

REFUND |

24 |

|

||

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

00

Under penalties of perjury, I declare to the best of my knowledge and belief, this return and accompanying schedules are true, correct and complete.

SIGN |

Signature of fiduciary or officer representing estate or trust |

Date |

EIN of administrator of fiduciary |

|

|

Enter "X" if the Tax Commission may |

||

|

|

|

|

|

|

|

discuss this return with preparer |

|

HERE |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

shown below (see page 12) |

|

|

|

|

|

|

|

|

|

|

|

|

|

Preparer' s signature (page 12) |

Date |

Preparer' s telephone number |

|

Preparer' s Social Security no. or PTIN |

|

Paid |

|

|

|

|

|

|

||

Preparer’s |

|

|

|

|

|

|

|

|

|

Firm' s name and address |

|

|

|

Preparer' s EIN |

|||

Section |

|

|

|

|||||

|

|

|

|

|

|

|||

|

|

|

|

|

|

|

|

|

Mail this return and any payment due (with

41072

Schedule A – Nonresident Estate or Trust (computation of federal taxable income)

To be completed by all nonresident estates or trusts. |

|

1. Total income from federal form 1041 line 9 or |

|

2. Ordinary income derived from Utah sources (attach schedule - page 13) |

2 |

3. Utah capital gain or (loss) from Utah sources (attach schedule – page 13) |

3 |

4.Total income derived from Utah sources (add lines 2 and 3)

5.Percent of total federal income derived from Utah sources (line 4 divided by line 1 - not greater than 100%)

6.Deductions from federal form 1041or

7. Deductions from federal form 1041 or

8.Allocable amount (line 7 multiplied by line 5)

9.Total deductions allocable to Utah income (add lines 6 and 8)

10. Federal taxable income derived from Utah sources (line 4 less line 9). Enter here and on line 4 on front of form

1

00

00

4

5

6

00

8

9

10

00

00

%

00

00

00

00

Schedule S - Supplemental Schedule

PART 1: ADDITIONS TO INCOME (see codes and descriptions on page 4) |

PART 2: OTHER DEDUCTIONS (see codes and descriptions on page 5) |

Code |

Amount |

Code |

Amount |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

Total additions to income |

|

00 |

Total other deductions |

|

|

00 |

|

|

(enter total on page 1, line 5) |

|

(enter total on page 1, line 8) |

|

|

|

|||

|

|

|

If deducting Native American Income (code 77), write the |

|

|

|

||

|

|

|

enrollment number and tribe code. |

Tribe code |

||||

|

|

|

|

|

|

|||

|

|

|

Enrollment |

|

|

|

|

|

|

|

|

number |

|

|

|

|

|

PART 3: NONREFUNDABLE CREDITS (see codes and descriptions on page 7) |

PART 4: REFUNDABLE CREDITS (see codes and descriptions on page 10) |

||

Code |

Amount |

Code |

Amount |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

|

00 |

Total nonrefundable credits |

|

00 |

|

Total refundable credits |

|

|

00 |

||

(enter total on page 1, line12) |

|

|

(enter total on page 1, line 20) |

|

|

||||

|

|

|

|

|

|

||||

If claiming the Qualified Sheltered Workshop cash contribution |

If claiming the Nonresident Shareholder' s WithholdingTax |

||||||||

credit (code 02), write the Qualified Sheltered Workshop name. |

Credit (code 43), write the S corporation federal ID number. |

||||||||

Name |

|

|

|

|

FEIN |

|

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

PART 5: Credit for fiduciary income tax paid to another state (page 8). Enter code 17 and amount from line 7 below on Part 3, Nonrefundable Credits above. Complete a separate Part 5 for each state for which you are claiming a credit.

1. Total income taxed in state of: |

|

|

1 |

|

|||

2. Total income from federal form 1041 line 9 or |

2 |

||

3. Percent other state income bears to total income (line 1 divided by line 2 - not greater than 100%) |

3 |

||

4. Utah fiduciary tax as computed on line 11 on front of form |

4 |

||

5. Credit limitation (line 4 multiplied by percent on line 3) |

5 |

||

6. Fiduciary tax paid to state listed on line 1 |

6 |

||

7. Credit for fiduciary taxes paid to other state (line 5 or 6, whichever is less) Enter code 17 and credit on Sch. S, Part 3 above. |

7 |

||

00

00

%

00

00

00

00

Form 1041 - U.S. Income Tax Return for Estates and Trusts: This form is used by estates and trusts to report income, deductions, gains, and losses. Like the TC-41, it requires similar financial details, including income sources and deductions, to calculate the tax owed.

Form 1040 - U.S. Individual Income Tax Return: While this form is for individual taxpayers, both forms share the goal of reporting income and calculating tax liability. They require details about income, deductions, and credits, making them comparable in structure and purpose.

Missouri Notice to Quit: This form is crucial for landlords needing to request tenants to vacate the premises. For additional information and to access the form, please refer to the Missouri PDF Forms.

Form 990 - Return of Organization Exempt from Income Tax: Nonprofit organizations use this form to report their financial activities. Similar to the TC-41, it involves detailed reporting of income and expenses, although it focuses on tax-exempt entities rather than fiduciary income.

Form TC-548 - Utah Income Tax Credit for Taxes Paid to Another State: This form is used to claim a credit for taxes paid to another state. Like the TC-41, it is specific to Utah and involves calculations related to tax liabilities, making them closely related in function.

Form W-2 - Wage and Tax Statement: Employers use this form to report wages paid to employees and the taxes withheld. The TC-41 also requires reporting of income, although it is focused on fiduciary entities. Both forms play a crucial role in the overall tax reporting process.

The Utah TC-41 form is essential for fiduciary income tax returns in the state. Here are key takeaways to keep in mind when filling out and using this form: