Blank Utah Tc 559 Form

Blank Utah Tc 559 Form

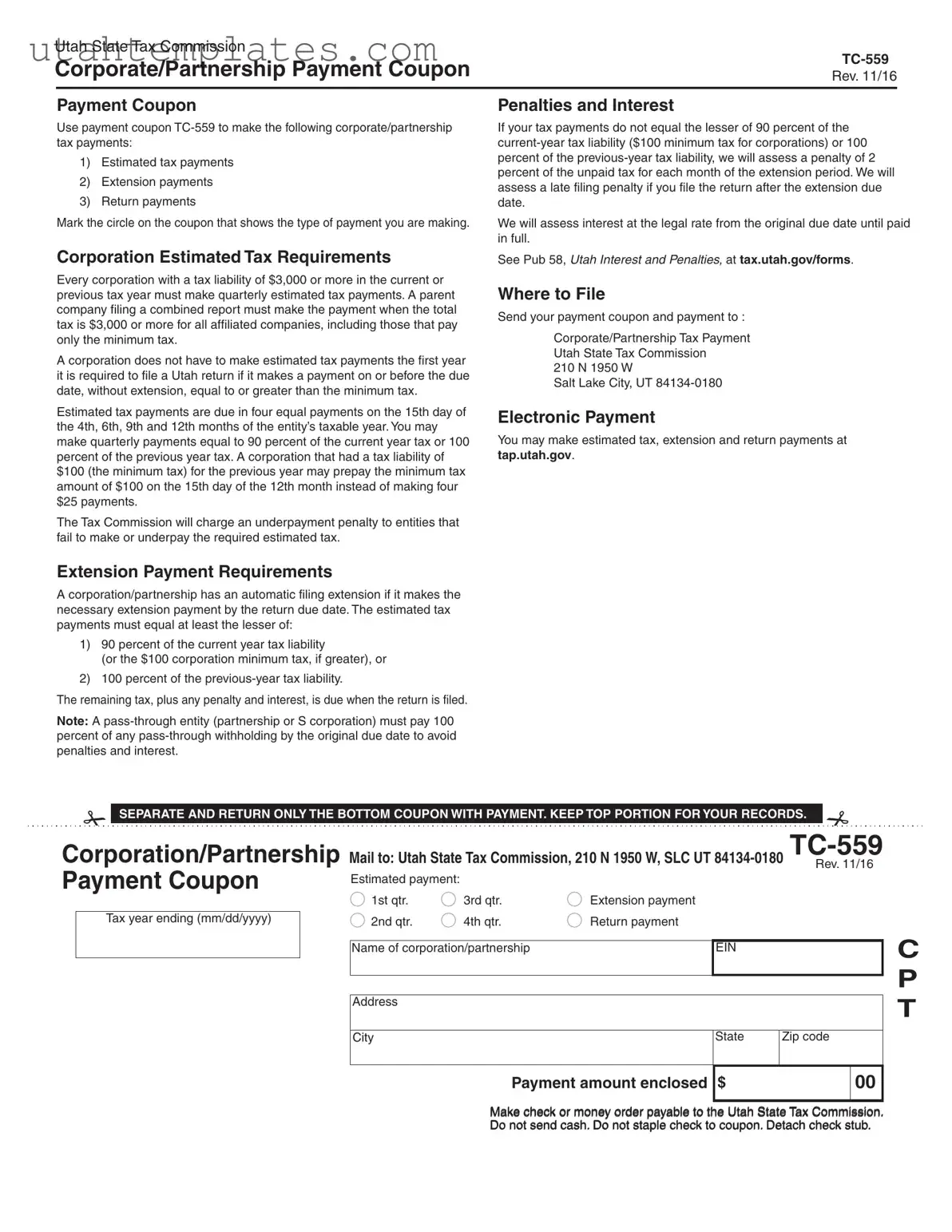

The Utah TC-559 form serves as an essential tool for corporations and partnerships in managing their tax obligations within the state. This payment coupon is utilized for various types of tax payments, including estimated tax payments, extension payments, and return payments. Taxpayers must indicate the type of payment they are making by marking the appropriate circle on the form. Understanding the implications of failing to meet tax obligations is crucial, as penalties and interest may apply. For instance, if tax payments do not meet specific thresholds—either 90 percent of the current-year tax liability or 100 percent of the previous-year tax liability—a penalty of 2 percent of the unpaid tax may be assessed for each month of the extension period. Additionally, a late filing penalty can be incurred if the return is submitted after the extension due date. Corporations with a tax liability of $3,000 or more are required to make quarterly estimated tax payments, with specific due dates throughout the taxable year. Furthermore, the TC-559 form outlines the requirements for extension payments, which allow corporations and partnerships an automatic filing extension when the necessary payment is made by the return due date. To avoid penalties and interest, it is important for pass-through entities to pay any withholding by the original due date. Finally, taxpayers can submit their payment coupon and payment to the Utah State Tax Commission, either by mail or electronically, ensuring compliance with state tax regulations.

Medical Power of Attorney Utah - This directive can facilitate discussions about complex medical decisions.

Completing the sale of your motorcycle in Illinois requires careful attention to detail, and using the Illinois Motorcycle Bill of Sale form ensures that both the seller and buyer are protected. This form not only validates the transaction but also provides necessary details regarding the motorcycle. To efficiently navigate this process, make sure to access and download the form to facilitate your transaction smoothly.

Utah Cpe - It is important to keep copies of submitted forms for your records.

| Fact Name | Details |

|---|---|

| Purpose of TC-559 | The TC-559 form is used by corporations and partnerships in Utah to make various tax payments, including estimated tax payments, extension payments, and return payments. |

| Payment Requirements | Corporations must make quarterly estimated tax payments if their tax liability is $3,000 or more. Payments are due on the 15th of the 4th, 6th, 9th, and 12th months of the taxable year. |

| Penalties and Interest | If tax payments do not meet the required thresholds, penalties of 2% per month may apply. Interest is also charged from the original due date until the tax is paid in full. |

| Governing Law | This form is governed by the Utah State Tax Commission regulations, specifically outlined in Utah Code Title 59, Chapter 7, regarding corporate taxes. |

When dealing with the Utah TC-559 form, several other forms and documents may come into play. These documents help ensure compliance with tax obligations and streamline the filing process for corporations and partnerships. Here’s a list of some commonly used forms alongside the TC-559:

Understanding these forms can simplify the tax filing process and help avoid potential penalties. Each document serves a unique purpose and is essential for maintaining compliance with Utah tax laws. Keeping these forms organized and readily accessible will make tax season less stressful.

Filling out the Utah TC-559 form correctly is crucial for avoiding unnecessary penalties and ensuring compliance with tax regulations. One common mistake is failing to mark the correct payment type. The form requires you to indicate whether you are making an estimated tax payment, an extension payment, or a return payment. Neglecting to circle the appropriate option can lead to confusion and delays in processing your payment.

Another frequent error involves miscalculating the payment amount. Taxpayers often overlook the requirement that estimated tax payments must equal at least 90 percent of the current year's tax liability or 100 percent of the previous year's tax liability. If the payment is less than these amounts, a penalty of 2 percent may be assessed for each month of the extension period. Thus, it is vital to double-check calculations to avoid unnecessary penalties.

People also often forget to pay attention to the due dates for estimated tax payments. These payments are due quarterly on specific dates throughout the year. Missing a due date not only results in penalties but may also complicate your overall tax situation. Mark your calendar and ensure that payments are submitted on time to avoid these issues.

Another mistake involves improper submission of the payment coupon. Taxpayers sometimes send the entire form instead of detaching the bottom coupon as instructed. This can lead to processing delays or even lost payments. Always remember to separate and return only the bottom coupon with your payment while keeping the top portion for your records.

Lastly, many individuals overlook the importance of including accurate identifying information. It is essential to fill in the name of the corporation or partnership, the Employer Identification Number (EIN), and the address correctly. Errors in this information can lead to misallocation of payments and potential penalties. Ensure that all fields are completed accurately to facilitate smooth processing.

Utah State Tax Commission

Corporate/Partnership Payment Coupon |

|

Rev. 11/16 |

|

|

|

Payment Coupon |

Penalties and Interest |

Use payment coupon

1)Estimated tax payments

2)Extension payments

3)Return payments

Mark the circle on the coupon that shows the type of payment you are making.

If your tax payments do not equal the lesser of 90 percent of the

We will assess interest at the legal rate from the original due date until paid in full.

Corporation Estimated Tax Requirements

Every corporation with a tax liability of $3,000 or more in the current or previous tax year must make quarterly estimated tax payments. A parent company filing a combined report must make the payment when the total tax is $3,000 or more for all affiliated companies, including those that pay only the minimum tax.

A corporation does not have to make estimated tax payments the first year it is required to file a Utah return if it makes a payment on or before the due date, without extension, equal to or greater than the minimum tax.

Estimated tax payments are due in four equal payments on the 15th day of the 4th, 6th, 9th and 12th months of the entity’s taxable year. You may make quarterly payments equal to 90 percent of the current year tax or 100 percent of the previous year tax. A corporation that had a tax liability of $100 (the minimum tax) for the previous year may prepay the minimum tax amount of $100 on the 15th day of the 12th month instead of making four $25 payments.

The Tax Commission will charge an underpayment penalty to entities that fail to make or underpay the required estimated tax.

Extension Payment Requirements

A corporation/partnership has an automatic filing extension if it makes the necessary extension payment by the return due date. The estimated tax payments must equal at least the lesser of:

1)90 percent of the current year tax liability

(or the $100 corporation minimum tax, if greater), or

2)100 percent of the

The remaining tax, plus any penalty and interest, is due when the return is filed.

Note: A

See Pub 58, UTAH INTEREST AND PENALTIES, at tax.utah.gov/forms.

Where to File

Send your payment coupon and payment to :

Corporate/Partnership Tax Payment

Utah State Tax Commission

210 N 1950 W

Salt Lake City, UT

Electronic Payment

You may make estimated tax, extension and return payments at tap.utah.gov.

SEPARATE AND RETURN ONLY THE BOTTOM COUPON WITH PAYMENT. KEEP TOP PORTION FOR YOUR RECORDS.

Corporation/Partnership Mail to: Utah State Tax Commission, 210 N 1950 W, SLC UT |

||||||||

Rev. 11/16 |

||||||||

Payment Coupon |

|

Estimated payment: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1st qtr. |

3rd qtr. |

Extension payment |

|

|

|

|

|

|

|

|

|

|

|

|

|

Tax year ending (mm/dd/yyyy) |

|

2nd qtr. |

4th qtr. |

Return payment |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

Name of corporation/partnership |

|

EIN |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Address |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

City |

|

|

State |

Zip code |

|

|

|

|

|

|

|

|

|

|

C P T

Payment amount enclosed

$

00

Make check or money order payable to the Utah State Tax Commission. Do not send cash. Do not staple check to coupon. Detach check stub.

Understanding the Utah TC-559 form is essential for corporations and partnerships to ensure compliance with state tax regulations. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the process of filling out and submitting the TC-559 form with greater confidence. Ensuring timely and accurate payments can help you avoid unnecessary penalties and interest, allowing you to focus on your business operations.