Blank Utah Tc 65 Form

Blank Utah Tc 65 Form

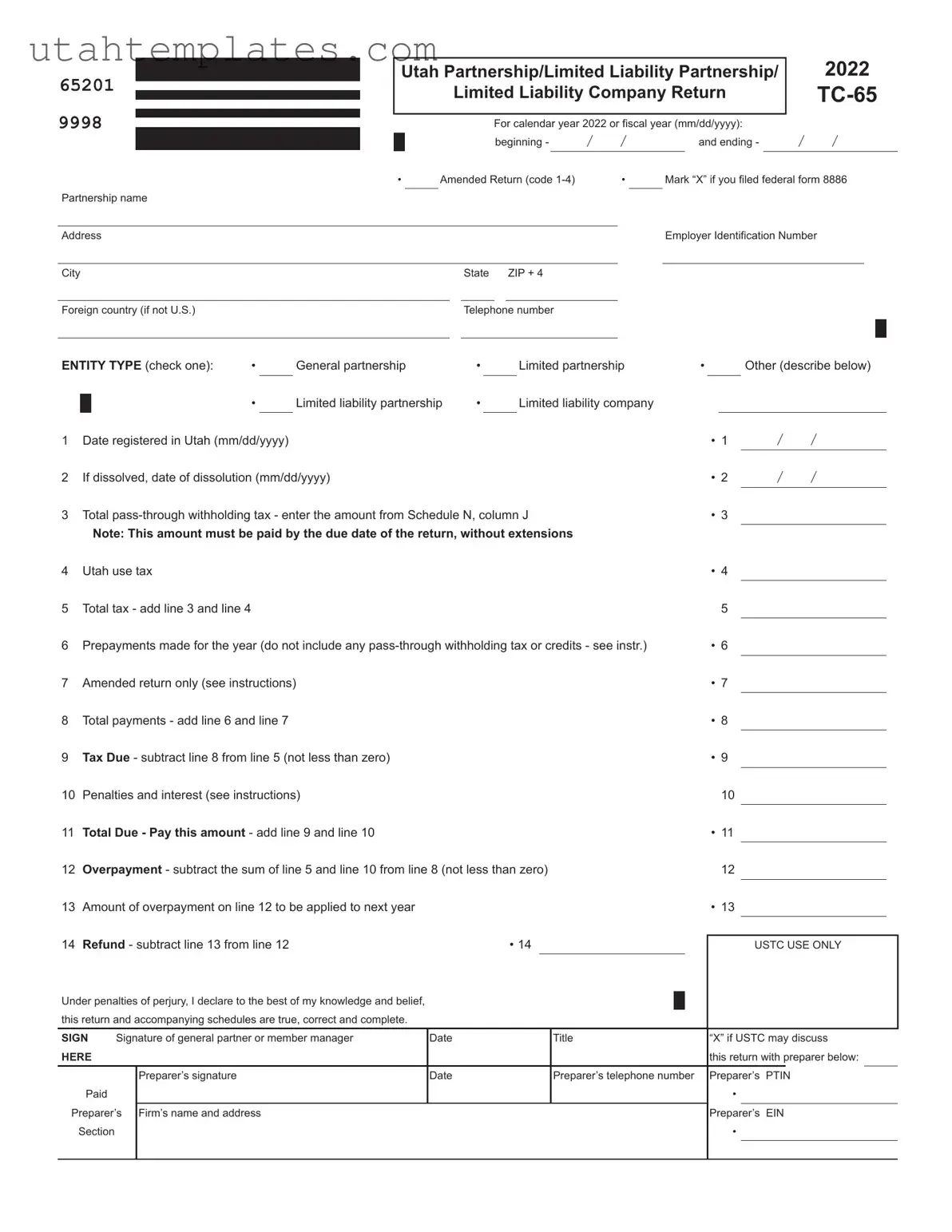

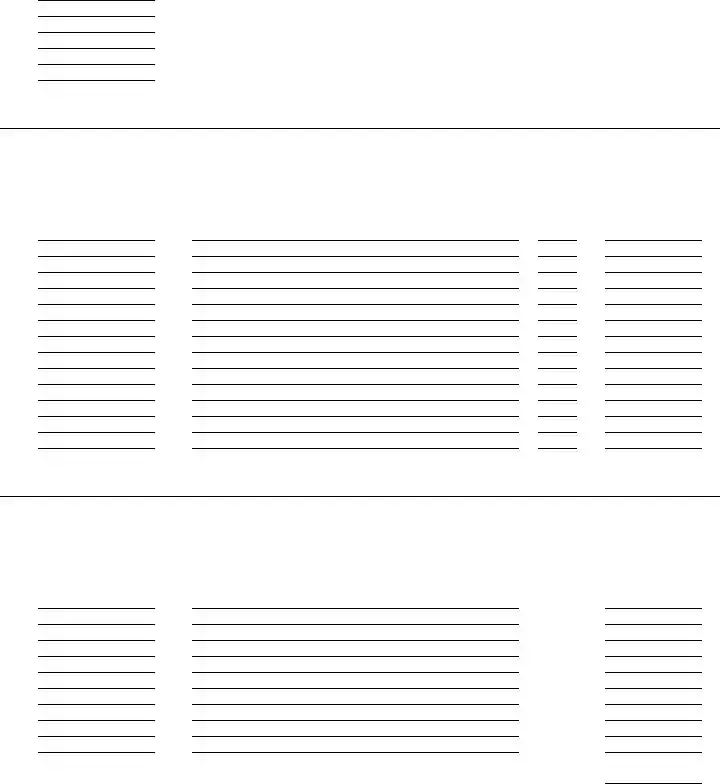

The Utah TC-65 form is an essential document for partnerships and limited liability companies operating in Utah. It serves as the official return for reporting income, deductions, and tax liabilities for these entities. This form is specifically designed for the calendar year 2020 or for a fiscal year defined by the entity. It includes sections for general information, such as the partnership's name, address, and Employer Identification Number (EIN). Additionally, the TC-65 requires the entity to specify its type—whether it is a general partnership, limited partnership, limited liability partnership, or limited liability company. The form also incorporates various financial details, including total pass-through withholding tax, Utah use tax, and total tax due. Notably, it provides a mechanism for reporting any prepayments made during the year, penalties, and interest, as well as the calculation of any overpayments or refunds. Furthermore, the TC-65 includes schedules for detailing Utah taxable income, nonbusiness income, and apportionment factors, ensuring that all relevant financial information is accurately reported. Completing the TC-65 correctly is crucial for compliance with Utah tax regulations and for determining the entity's tax obligations.

Does Utah Tax Social Security - Nonrefundable credits can be claimed on the TC-41 form to reduce tax liability.

For those looking to create a Bill of Sale in Pennsylvania, it's important to have the right resources at hand. This form not only validates the transfer of ownership but also helps both parties in maintaining clear records of their transaction. To find a suitable template, you can visit legalformspdf.com, which offers essential information and forms necessary for a smooth sale process.

Utah Real Estate Forms - The addendum must be signed and dated by both parties for validation.

| Fact Name | Description |

|---|---|

| Form Purpose | The TC-65 form is used by partnerships, limited liability partnerships, and limited liability companies in Utah to report their income and calculate taxes for the year. |

| Filing Requirement | Entities must file this form annually, either for a calendar year or a fiscal year, depending on their accounting period. |

| Governing Law | The TC-65 form is governed by Utah state tax laws, specifically under the Utah Code Title 59, Chapter 7. |

| Entity Types | Filing entities can select from various types, including general partnerships, limited partnerships, limited liability partnerships, and limited liability companies. |

| Withholding Tax | Entities must report total pass-through withholding tax on the form, which is due by the return's filing deadline. |

| Amended Returns | If there are changes to the originally filed return, entities can indicate that they are submitting an amended return by marking the appropriate box. |

| Payment Information | Entities must calculate total tax due, prepayments made, and any penalties or interest, ensuring they pay the correct amount by the deadline. |

| Signature Requirement | The form must be signed by a general partner or member manager, affirming that the information provided is accurate and complete. |

The Utah TC-65 form is an important document used by partnerships and limited liability companies to report income and taxes. Several other forms and documents are often used alongside it to ensure accurate reporting and compliance with state tax regulations. Below is a list of these related documents.

Using these forms and documents in conjunction with the TC-65 helps ensure that partnerships and limited liability companies meet their tax obligations accurately and efficiently. Proper completion of all relevant forms can prevent potential issues with state tax authorities.

Filling out the Utah TC-65 form can be challenging, and many individuals make common mistakes that can lead to delays or issues with their tax returns. One frequent error is failing to provide accurate information regarding the partnership or limited liability company's name and address. It is essential to ensure that the name matches exactly with what is registered with the state. Any discrepancies can cause confusion and may result in the return being rejected.

Another common mistake is neglecting to indicate the correct entity type. The form requires the filer to check the appropriate box for the type of entity, such as a general partnership or limited liability company. If this step is overlooked, it can lead to misclassification and complications in processing the return.

Many filers also forget to include the Employer Identification Number (EIN). This number is crucial for identifying the business and is required on the form. Without it, the return may be considered incomplete, causing delays in processing or potential penalties.

Additionally, failing to report the total pass-through withholding tax accurately can lead to significant issues. This amount must be calculated correctly and entered on the appropriate line. Errors in this calculation can affect the total tax due and create complications with state tax authorities.

Finally, some individuals overlook the importance of signing the form. A signature is required to validate the return, and without it, the submission may not be accepted. It is vital to ensure that the general partner or member manager signs and dates the form before submission.

65201

9998

USTC ORIGINAL FORM

Partnership name

Address

City

Utah Partnership/Limited Liability Partnership/ |

|

2022 |

||||||||||

|

|

Limited Liability Company Return |

|

|||||||||

|

|

For calendar year 2022 or fiscal year (mm/dd/yyyy): |

|

|

|

|||||||

|

|

beginning - |

/ |

/ |

|

|

and ending - |

/ |

/ |

|

||

|

|

|

|

|

||||||||

|

|

|

|

|

|

|

|

|

|

|

||

• |

|

Amended Return (code |

|

• |

Mark “X” if you filed federal form 8886 |

|||||||

|

|

|

|

|

|

|

Employer Identification Number |

|

|

|||

|

|

|

|

|

|

|

|

|

||||

|

|

State ZIP + 4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Foreign country (if not U.S.)Telephone number

ENTITY TYPE (check one): |

• |

General partnership |

• |

|

Limited partnership |

• |

|

Other (describe below) |

|||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

• |

Limited liability partnership |

• |

|

Limited liability company |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1 |

Date registered in Utah (mm/dd/yyyy) |

|

|

|

|

|

|

• 1 |

/ |

/ |

|||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

2 |

If dissolved, date of dissolution (mm/dd/yyyy) |

|

|

|

|

|

• 2 |

/ |

/ |

||||||

3 |

Total |

|

• 3 |

|

|

|

|||||||||

|

|

|

|

||||||||||||

|

|

Note: This amount must be paid by the due date of the return, without extensions |

|

|

|

|

|

|

|||||||

|

|

|

|

|

|

|

|

||||||||

4 |

Utah use tax |

|

|

|

|

|

|

|

|

• 4 |

|

|

|

||

5 |

Total tax - add line 3 and line 4 |

|

|

|

|

|

|

|

5 |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

||||||

6 |

Prepayments made for the year (do not include any |

|

• 6 |

|

|

|

|||||||||

|

|

|

|

||||||||||||

7 |

Amended return only (see instructions) |

|

|

|

|

|

• 7 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

8 |

Total payments - add line 6 and line 7 |

|

|

|

|

|

|

• 8 |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|||||||

9 |

Tax Due - subtract line 8 from line 5 (not less than zero) |

|

|

|

|

|

• 9 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

10 |

Penalties and interest (see instructions) |

|

|

|

|

10 |

|

|

|

||||||

|

|

|

|

|

|

|

|||||||||

11 |

Total Due - Pay this amount - add line 9 and line 10 |

|

|

|

|

|

• 11 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

12 |

Overpayment - subtract the sum of line 5 and line 10 from line 8 (not less than zero) |

12 |

|

|

|

||||||||||

|

|

|

|||||||||||||

13 |

Amount of overpayment on line 12 to be applied to next year |

|

|

|

|

|

• 13 |

|

|

|

|||||

|

|

|

|

|

|

|

|

||||||||

14 |

Refund - subtract line 13 from line 12 |

|

|

• 14 |

|

|

|

|

|

||||||

|

|

|

|

|

|

USTC USE ONLY |

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Under penalties of perjury, I declare to the best of my knowledge and belief, |

|

|

|

|

|

|

|

|

|

||

this return and accompanying schedules are true, correct and complete. |

|

|

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

||||

SIGN |

Signature of general partner or member manager |

Date |

Title |

“X” if USTC may discuss |

|||||||

HERE |

|

|

|

|

|

|

this return with preparer below: |

||||

|

|

|

|

|

|

|

|

|

|

||

|

|

Preparer’s signature |

Date |

Preparer’s telephone number |

Preparer’s |

PTIN |

|||||

Paid |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

Preparer’s |

Firm’s name and address |

|

|

|

|

Preparer’s |

EIN |

||||

Section |

|

|

|

|

|

|

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule A - Utah Taxable Income for |

||||||

65202 |

EIN |

|

|

2022 |

|

|

||

USTC ORIGINAL FORM |

|

|

|

|

||||

1 |

Net income/loss from federal form 1065, Schedule K, Analysis of Net Income (Loss), line 1 |

• 1 |

||||||

|

|

|

|

|

|

|||

2 |

Contributions from federal form 1065, Schedule K, line 13a |

• 2 |

||||||

|

|

|

|

|

|

|||

3 |

Foreign taxes from federal form 1065, Schedule K, line 21 |

• 3 |

||||||

|

|

|

|

|

|

|||

4 |

Recapture of Section 179 deduction from all federal Schedules |

• 4 |

||||||

|

|

|

|

|

|

|||

5 |

Payroll Protection Program grant or loan addback (see instructions) |

• 5 |

||||||

|

|

|

|

|

|

|||

6 |

(Reserved, see instructions) |

• 6 |

||||||

7 |

Total income/loss - add lines 1 through 6 |

7 |

|

|

|

|||

|

|

|

||||||

|

|

|

|

|

|

|||

8 |

Total guaranteed payments to partners (see instructions) |

• 8 |

||||||

|

|

|

|

|

|

|||

9 |

Health insurance included in guaranteed payments on line 8 |

• 9 |

||||||

10 |

Net guaranteed payments to partners - subtract line 9 from line 8 |

10 |

|

|

|

|||

|

|

|

||||||

|

|

|

|

|

||||

11 |

Utah net nonbusiness income from |

• 11 |

||||||

|

|

|

|

|

|

|||

12 |

• 12 |

|||||||

13 |

Add lines 10 through 12 |

13 |

|

|

|

|||

|

|

|

||||||

|

|

|

|

|

||||

14 |

Apportionable income/loss - subtract line 13 from line 7 |

• 14 |

||||||

|

|

|

|

|

||||

15 |

Apportionment fraction - enter 1.000000, or |

• 15 |

||||||

|

|

|

|

|

|

|||

16 |

Utah apportioned business income/loss - multiply line 14 by line 15 |

• 16 |

||||||

|

|

|

|

|

||||

17 |

Total Utah income/loss allocated to |

• 17 |

||||||

|

|

|

|

|

|

|

|

|

Schedule H - Utah Nonbusiness Income Net of Expenses |

Pg. 1 |

|||||

20261 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Failure to complete this form may result in disallowance of the nonbusiness income. |

|

|

|

|

|||||||

Part 1 - Utah Nonbusiness Income (nonbusiness income allocated to Utah) |

|

|

|

|

|||||||

|

|

|

|

||||||||

|

|

|

|

||||||||

|

A |

B |

|

|

C |

D |

|

E |

|||

|

Type of Utah |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

Utah Nonbusiness Income |

||||

|

Nonbusiness Income |

Utah Nonbusiness |

|

Used to Produce Utah |

Used to Produce Utah |

|

|

|

|||

|

|

|

Asset(s) |

|

|

Nonbusiness Income |

Nonbusiness Income |

|

|

|

|

1a |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1b |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1c |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1d |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

1e |

/ |

/ |

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

2Total of column C and column D

3Total Utah nonbusiness income - add column E for lines 1a through 1e

|

Description of direct expenses related to: |

Amount of Direct Expense |

||

4a |

Line 1a above |

|

||

|

|

|

|

|

4b |

Line 1b above |

|

||

|

|

|

|

|

4c |

Line 1c above |

|

||

|

|

|

|

|

4d |

Line 1d above |

|

||

|

|

|

|

|

4e |

Line 1e above |

|

||

|

|

|

|

|

5Total direct related expenses - add lines 4a through 4e

6 |

Utah nonbusiness income net of direct related expenses - subtract line 5 from line 3 |

|

• |

||

|

|

Column A |

Column B |

||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

||

|

Utah Nonbusiness Income |

Utah Nonbusiness Income |

|

|

|

7 |

|

|

|

|

|

|

(enter in Column A the amount from line 2, col. C) |

|

|

|

|

|

|

|

|

|

|

8

(enter in Column A the amount from line 2, col. D)

9Sum of beginning and ending asset values (add line 7 and line 8)

10Average asset value - divide line 9 by 2

11Utah nonbusiness assets ratio - line 10, Column A, divided by line 10, Column B (to four decimal places)

12Interest expense deducted in computing Utah taxable income (see instructions)

13Indirect related expenses for Utah nonbusiness income - multiply line 11 by line 12

14 Total Utah nonbusiness income net of expenses - subtract line 13 from line 6 |

|

• |

|

Enter on: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule H - |

Pg. 2 |

|||||

20262 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Part 2 -

|

A |

B |

|

|

C |

D |

|

E |

||

|

Type of |

Acquisition Date of |

|

Beginning Value of Investment |

Ending Value of Investment |

|

||||

|

Nonbusiness Income |

|

|

Used to Produce |

Used to Produce |

|

Income |

|||

|

|

|

Nonbusiness Asset(s) |

|

Nonbusiness Income |

Nonbusiness Income |

|

|

||

15a |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15b |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15c |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15d |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

15e |

/ |

/ |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

16Total of column C and column D

17Total

|

Description of direct expenses related to: |

|

|

|

|

|

Amount of Direct Expense |

|

18a |

Line 15a above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18b |

Line 15b above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18c |

Line 15c above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18d |

Line 15d above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18e |

Line 15e above |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 |

Total direct related expenses - add lines 18a through 18e |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

20 |

• |

|||||||

|

|

|

Column A |

Column B |

|

|

||

|

|

|

|

|

||||

|

Indirect Related Expenses for |

Total Assets Used to Produce |

Total Assets |

|

|

|||

|

|

|

|

|

||||

21 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. C) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

22 |

|

|

|

|

|

|

||

|

(enter in Column A the amount from line 16, col. D) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

23Sum of beginning and ending asset values (add line 21 and line 22)

24Average asset value - divide line 23 by 2

25

26Interest expense deducted in computing

27Indirect related expenses for

28 Total |

• |

|

Enter on: |

|

|

|

|

|

|

|

|

Schedule J - Apportionment Schedule |

Pg. 1 |

|||||

20263 EIN |

|

|

|

|

2022 |

|

USTC ORIGINAL FORM |

|

|

(use with |

|

||

|

|

|

|

|

|

|

Note: Use this schedule only if the entity does business in Utah and one or more other states and income must be apportioned to Utah.

Briefly describe the nature and location(s) of your Utah business activities:

Apportionable Income Factors

|

|

|

|

|

Column A |

|

Column B |

|||

1 |

Property Factor |

|

|

Inside Utah |

|

Inside and Outside Utah |

||||

|

a |

Land |

• 1a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

b |

Depreciable assets |

• 1b |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Inventory and supplies |

• 1c |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Rented property |

• 1d |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Other allowable property (see instructions) |

• 1e |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

f |

Total tangible property - add lines 1a through 1e |

• 1f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

2 |

Property factor - divide line 1f, Column A, by line 1f, Column B (to six decimal places) |

• |

2 |

|

|

|

||||

3 |

Payroll Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total wages, salaries, commissions and other compensation |

• 3a |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

||

4 |

Payroll factor - divide line 3a, Column A, by line 3a, Column B (to six decimal places) |

• |

4 |

|

|

|

||||

5 |

Sales Factor |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

|

a |

Total sales (gross receipts less returns and allowances) |

|

|

|

• |

5a |

|||

|

b |

Sales delivered or shipped to Utah buyers from outside Utah |

• 5b |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

c |

Sales delivered or shipped to Utah buyers from within Utah |

• 5c |

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

d |

Sales shipped from Utah to the United States government |

• 5d |

|

|

|

|

|

||

|

|

|

|

|

|

|||||

|

|

|

|

|

|

|

|

|

|

|

|

e |

Sales shipped from Utah to buyers in states where the corp. |

• 5e |

|

|

|

|

|

||

|

|

has no nexus (corporation not taxable in buyer’s state) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

f |

Rent and royalty income |

• 5f |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

g |

Services and other allowable sales (see instructions) |

• 5g |

• |

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

|

|

h |

Total sales (add lines 5a through 5g) |

• 5h |

• |

|

|

|

|

||

|

|

|

|

|

|

|

||||

6 Sales factor - line 5h, Column A, divided by line 5h, Column B (to six decimals) |

• |

6 |

|

|

|

|||||

|

|

Continued on page 2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Schedule J - Apportionment Schedule |

Pg. 2 |

|||||

20264 EIN |

|

|

2022 |

|

|

|

||

USTC ORIGINAL FORM |

(use with |

|

|

|||||

|

|

|

|

|

|

|

||

|

|

|

|

|

|

|

|

|

|

7 All entities - enter your NAICS code here (see instructions) |

• 7 |

|

|

||||

Apportionment Fraction |

|

|

|

|

||||

|

|

|

|

|||||

|

Optional apportionment taxpayers (see instructions) complete Part 1 or Part 2. |

|

|

|

|

|||

|

Sales factor weighted taxpayers (see instructions) complete Part 2. |

|

|

|

|

|||

Part 1:

8 |

Total factors - add lines 2, 4 and 6 |

|

8 |

9 |

Calculate the Apportionment Fraction to SIX DECIMALS |

• |

9 |

|

Divide line 8 by 3 (or the number of factors present) |

|

|

Part 2: Sales Factor Formula (see instructions for those who qualify) |

|

|

|

10 |

Apportionment Fraction - enter the |

• |

10 |

Enter the fraction from line 9 or line 10, above, as follows:

Schedule K - Partners’ Distribution Share Items |

|

|

|||

65203 EIN |

|

|

2022 |

||

USTC ORIGINAL FORM |

|

|

|

||

Number of Schedules |

• |

||||

|

|

|

|

|

|

Income/Loss

Deductions

Utah Credits

Federal Amount |

Utah Amount |

1Ordinary business income/loss

2Net rental real estate income/loss

3 Other net rental income/loss

4 Guaranteed payments

5a U.S. government interest income

5b Municipal bond interest income

5c Other interest income

6Ordinary dividends

7 Royalties

8 Net

9 Net

10 Net Section 1231 gain/loss

11 Recapture of Section 179 deduction

12 Other income/loss (describe)

13Section 179 deduction

14Contributions

15Foreign taxes paid or accrued

16Other deductions (describe)

17 Utah nonrefundable credits - enter the name of the Utah credit |

Code |

|

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18 Utah refundable credits - enter the name of the Utah credit |

Code |

|

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19 Total Utah tax withheld on behalf of all partners from Schedule N, column J

|

Schedule |

|

65204 |

of Utah Income, Deductions and Credits |

2022 |

USTC ORIGINAL FORM

Partnership Information

APartnership’s EIN:

BPartnership’s name, address, city, state, and ZIP code

Partner Information

C Partner’s SSN or EIN:

D Partner’s name, address, city, state, and ZIP code

EPartner’s phone number

F Percent of ownership

G Enter “X” if limited partner or member

H Entity code from list below: |

|

|

|

|

|

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

I = Individual |

|

|

P = Gen’l Partnership |

|

|

||||||

|

C = Corporation |

|

L = Limited Partnership |

|

|

|||||||

|

Codes |

|

|

|

||||||||

|

S = S Corporation |

|

B = LLC |

|

|

|

|

R = LLP |

||||

|

N = Nonprofit Corp. |

|

T = Trust |

|

|

|

|

O = Other |

||||

|

|

|

|

|

|

|

||||||

I |

Enter date: |

|

/ |

/ |

/ |

/ |

|

|||||

|

|

|

|

|

|

|

|

|

|

|

||

|

|

|

|

affiliated |

|

|

|

|

withdrawn |

|||

|

|

|

|

|

|

|

|

|

||||

Partner’s Share of Apportionment Factors |

|

|

|

|

|

|

|

|||||

|

|

|

|

|

Utah |

|

|

|

|

|

Total |

|

J |

Property |

$ |

|

|

$ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

||

K |

Payroll |

$ |

|

|

$ |

|

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

L |

Sales |

|

$ |

|

|

$ |

|

|

|

|||

|

|

|

|

|

|

|

|

|

|

|

|

|

Other Information

Note: To complete lines 1 through 16:

*Utah residents, enter the amounts from federal Schedule

*Utah nonresidents, see instructions to calculate amounts.

All filers complete lines 17 through 19, if applicable.

Partner’s Share of Utah Income, Deductions and Credits

1Utah ordinary business income/loss

2Utah net rental real estate income/loss

3 Utah other net rental income/loss

4 Utah guaranteed payments

5a Utah U.S. government interest income

5b Utah municipal bond interest income

5c Utah other interest income

6Utah ordinary dividends

7 Utah royalties

8 Utah net

9 Utah net

10 Utah net Section 1231 gain/loss

11 Utah recapture of Section 179 deduction

12 Utah other income/loss (describe)

13Utah Section 179 deduction

14Contributions

15Foreign taxes paid or accrued

16Utah other deductions (describe)

17Utah nonrefundable credits:

Name of Credit |

Code |

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

18 Utah refundable credits:

Name of Credit |

Code |

Credit Amount |

||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

19Utah tax withheld on behalf of partner “X” if withholding waiver applied for

Schedule N - |

|

|||

65205 EIN |

|

|

|

2022 |

USTC ORIGINAL FORM

A partnership with nonresident individual partners, resident/nonresident business partners, or resident/nonresident trust or estate partners must complete the information below to calculate the Utah withholding tax for these partners. See instructions for column G, column H and column I.

WITHHOLDING WAIVER CLAIMED under |

|

• |

|||||||||||||||||||||||||||

Enter "1" to claim a waiver for ALL partners (enter "X" in column B and "0" in column F for all partners) |

|

|

|

|

|

|

|

|

|

|

|

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

Enter "2" to claim a waiver for SOME partners (enter "X" in column B and "0" in column F for those partners claimed) |

|

|

|

|

|

|

|||||||||||||||||||||||

|

|

|

|

|

|

||||||||||||||||||||||||

|

See Schedule N instructions for liability responsibilities when claiming a waiver. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||

A |

Name of partner |

|

|

|

|

E |

Income/loss |

F |

4.85% of income - |

G |

Mineral production |

J Withholding tax |

|||||||||||||||||

B |

Withholding waiver for this partner |

|

|

attributable to Utah |

|

|

E times .0485 |

|

|

|

withholding credit |

|

to be paid by |

||||||||||||||||

|

(enter “X” in column B and “0” in column F) |

|

|

plus Utah source |

|

|

(not less than zero) H |

|

this partnership |

||||||||||||||||||||

C |

SSN or EIN of partner |

|

|

|

|

|

|

guaranteed pymts |

|

|

|

|

|

|

|

through withholding |

|

F less G, H and I |

|||||||||||

D |

Partner’s % of income or ownership |

|

|

(see instructions) |

|

|

|

|

I Tax paid by PTE |

|

(not less than 0) |

||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

#1 |

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

|||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#2 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#3 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#4 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|||||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#5 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#6 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

#7 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||

A |

|

|

|

|

|

E |

|

|

|

|

F |

|

|

G |

|

|

J |

||||||||||||

• |

B |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

H |

|

|

|

|

|

|

|

|

|

|||

• |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

C |

D |

|

|

|

|

|

|

|

|

|

|

I |

|

|

|

|

|

|

|

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

||||

|

Report the partner’s |

|

|

|

|

Total Utah withholding tax to be paid by this partnership: |

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

|

tax from column J on Schedule |

|

|

|

|

Enter on |

|

|

|

|

|

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||

Credits Received from |

|||

25201 and Mineral Production Withholding Tax Credit on |

2022 |

||

EIN |

|

|

(use with |

USTC ORIGINAL FORM

Part 1 - Utah Nonrefundable Credits Received from

1

2

3

4

5

6

|

|

|

|

UT nonrefundable |

Name of |

|

Credit |

credit from |

|

from Utah Schedule |

|

Code |

Utah Sch. |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Enter these credits on Utah

Part 2 - Utah Refundable Credits Received from

Name of |

Credit |

UT refundable credit |

from Utah Schedule |

Code |

from Utah Sch. |

1

2

3

4

5

6

7

8

9

10

11

12

13

14

Enter these credits on Utah

Part 3 - Utah Mineral Production Withholding Tax Credit Received on

|

|

Mineral production |

Producer EIN from |

|

withholding from |

Producer’s name from |

1

2

3

4

5

6

7

8

9

10

Total Utah mineral production withholding tax credit received on

Enter total credit on Utah

Form 1065: This is the U.S. Return of Partnership Income. Like the TC-65, it reports the income, deductions, gains, and losses of a partnership. Both forms require detailed financial information about the partnership's operations and distributions to partners.

Form 1065 Schedule K-1: This document is used to report each partner's share of the partnership's income, deductions, and credits. Similar to TC-65, it provides a breakdown of financial information that is crucial for individual tax returns.

Indiana Homeschool Letter of Intent: This form is essential for families who wish to homeschool in Indiana. It officially notifies the state of their intent and ensures compliance with state regulations. For further details on how to complete this important document, visit homeschoolintent.com/editable-indiana-homeschool-letter-of-intent.

Form 8832: This form allows a partnership to elect how it will be classified for federal tax purposes. Like the TC-65, it involves decisions about the partnership's structure and tax treatment, impacting how income and losses are reported.

Form TC-20: This is the Utah Corporate Franchise or Income Tax Return. While TC-65 is for partnerships, TC-20 is for corporations. Both forms require reporting of state tax obligations and share similar structures for detailing income and expenses.

Filling out the Utah TC-65 form is a crucial step for partnerships and limited liability companies operating in Utah. Here are some key takeaways to consider when completing and utilizing this form:

By keeping these key points in mind, you can navigate the process of filling out the Utah TC-65 form with greater confidence and accuracy. Remember, attention to detail is critical in ensuring compliance and minimizing potential issues with your tax filings.